What Is Transfer Pricing in Hong Kong?

Transfer pricing is the practice of setting prices for goods, services, and intellectual property exchanged between related entities across borders. In Hong Kong, transfer pricing plays a critical role for businesses involved in cross-border transactions to ensure fair market practices and compliance with tax regulations. It serves to prevent tax evasion by rightly attributing profit relevant to each jurisdiction based on the value each entity provides.

Content Outline

Key Summary

Ensures Fair Profit Allocation Across Borders

Transfer pricing assigns profits appropriately to different jurisdictions based on the value each entity creates, preventing tax evasion.

Follows the Arm’s Length Principle

All intercompany transactions must be priced as if they were between independent parties, ensuring compliance with fair market practices.

Requires Comprehensive Documentation

Businesses must prepare Master Files, Local Files, and CbCR reports to demonstrate compliance with IRD guidelines and avoid penalties.

Penalties for Non-Compliance

The IRD can impose fines, conduct audits, and request additional documentation (e.g., Form I.R. 1475) if companies fail to meet compliance requirements.

Alignment with OECD and BEPS Frameworks

Hong Kong’s regulations follow global OECD guidelines, focusing on transparency, proper profit allocation, and the elimination of tax base erosion

Understanding the Basics of Transfer Pricing

The basic principle of transfer pricing is the arm’s length principle. This principle requires that related entities have to price their intercompany transactions as independent parties would under comparable conditions. For instance, if a Hong Kong-based subsidiary sells products to a related entity in another country, the pricing must be at the fair market conditions to avoid manipulating profit allocations. Transfer pricing applied not only physical goods but also services, royalties, loans, and even intellectual property rights.

Hong Kong’s Transfer Pricing Regulations and Compliance Requirements

Hong Kong has also updated its laws and regulations to align with the OECD Transfer Pricing Guidelines. It requires companies to document transfer pricing practices to prove their compliance with rules and regulations.

Overview of the Inland Revenue Department (IRD) Guidelines

For Hong Kong, the Inland Revenue Department (IRD) enforces the regulations of transfer pricing through various directives including DIPN 46 (dipn46). It ensures that companies engaged in cross-border related party transactions maintain records demonstrating that their transactions comply with the arm’s-length principle.

Introduction to DIPN 46: Key Points for Taxpayers

DIPN 46 discusses guidelines on acceptable transfer pricing methods, the importance of maintaining comprehensive documentation, and justifying the pricing policy by benchmarking against independent parties. Businesses must ensure accurate records to avoid compliance risk and any potential audit challenge.

Transfer Pricing Documentation Requirements

Documentation is a key factor in proving compliance with Hong Kong transfer pricing regulations. Components are:

Master File & Local File: Who Needs to Prepare Them?

Companies meeting specific thresholds related to revenue, assets or employee numbers must prepare both the Master File and Local File. These documents respectively contain a company’s global transfer pricing policies and detailed local operations respectively.

Country-by-Country Reporting (CbCR)

CbCR applies to multinational enterprises (MNEs) with consolidated group revenue exceeding HK$6.8billion. This report provides tax authorities with a comprehensive view of the global allocation of income and taxes.

Deadlines for Transfer Pricing Documentation

The documentation should be prepared within 9 months after the end of the financial year. If these deadlines are not met, penalties by IRD can be imposed.

Transfer Pricing Methods Approved by the IRD

The IRD recognizes several methods for calculating transfer prices. Each method ensures that transactions reflect market-based pricing:

Comparable Uncontrolled Price (CUP) Method

Compares the price of a controlled transaction to what independent parties would charge for the same or similar product/service under similar conditions.

Resale Price Method

Calculates the arm’s length price by subtracting a resale margin from the final sale price to a third party, reflecting what a similar independent distributor would earn

Cost-Plus Method

Adds a reasonable markup to the supplier’s costs, ensuring the total price aligns with what independent suppliers charge for similar products or services.

Profit Split Method

Divides combined profits between related parties based on each party’s contribution, reflecting their respective roles and risks in the transaction

Transactional Net Margin Method (TNMM)

Compares the net profit margin from a controlled transaction to what independent companies earn in similar circumstances

| Method | How It Works | Best Use Cases | Challenges | Example |

| Comparable Uncontrolled Price (CUP) Method | Compares the price of controlled transactions (between related entities) with prices from independent parties in similar transactions. | Works best when there is reliable external or internal data on identical or similar products/services. | Finding appropriate comparables is difficult, especially when products have unique features. Adjustments are needed for differences in timing or market conditions. | A Hong Kong company sells electronic parts to both a third-party and a related subsidiary. If the prices are the same, it aligns with the arm’s length principle |

| Resale Price Method | Determines the transfer price by subtracting an appropriate resale margin from the final sale price to a third party. | Ideal for distributors or resellers that perform minimal value-adding activities. | Resale margins vary by industry and may be affected by factors such as marketing or logistics. | A Hong Kong distributor buys from a parent company and resells to retailers. The margin earned is compared to independent distributors in similar circumstances |

| Cost-Plus Method | Adds a markup to the costs incurred by the supplier to calculate the transfer price. | Commonly used for contract manufacturing or routine intra-group services. | Requires accurate cost tracking and reliable data on industry-standard markups. Allocation of overheads can be challenging. | A Hong Kong manufacturer provides goods to its overseas parent and applies a cost-based markup similar to independent manufacturers |

| Profit Split Method | Allocates the combined profits based on the relative contributions (functions, risks, and assets) of each party involved in the transaction. | Suitable for highly integrated operations or joint ventures, such as R&D collaborations. | Identifying the appropriate split factors and analyzing each party’s contribution can be complex. | A Hong Kong entity and a foreign affiliate jointly develop a product. Profits are split based on their respective R&D efforts and marketing activities |

| Transactional Net Margin Method (TNMM) | Evaluates the net profit margin relative to a financial indicator (e.g., sales or costs) and compares it with similar independent companies. | Preferred when gross margin data is unavailable or when one party performs routine functions with minimal risk. | Obtaining reliable data on net margins can be difficult. It assumes the tested party’s conditions align with those of independent companies. | A Hong Kong service provider charges a management fee to its parent company, and its net margin is compared with those of independent service providers |

Arm’s Length Principle: What It Means for Hong Kong Businesses

The arm’s length principle ensures that profits are taxed where value is created. Companies must provide evidence that their transfer prices align with this principle to avoid tax adjustments by the IRD.

Impact of Transfer Pricing on Cross-Border Transactions

Transfer pricing influences cross-border dealings by ensuring fair pricing between related entities. Companies with significant cross-border transactions must carefully manage their pricing strategies to comply with Hong Kong’s rules while minimizing tax exposure.

Penalties for Non-Compliance and Transfer Pricing Audits

Failure to maintain proper documentation can result in penalties, fines, and transfer pricing audits. The IRD actively monitors related party transactions and may issue Form I.R. 1475 to request further documentation.

Transfer Pricing And The OECD Guidelines

Hong Kong follows the OECD Transfer Pricing Guidelines, which are part of the global BEPS (Base Erosion and Profit Shifting) framework. Base Erosion and Profit Shifting (BEPS) refers to tax planning strategies used by multinational enterprises (MNEs) to exploit gaps and mismatches in international tax rules, shifting profits from higher-tax jurisdictions to lower-tax jurisdictions, thus eroding the taxable base. The OECD’s BEPS Action Plan aims to close these loopholes, ensuring that profits are taxed where economic activities and value creation occur.

How BEPS (Base Erosion and Profit Shifting) Impacts Compliance

- Increased Documentation Obligations

- MNEs must now provide Master Files, Local Files, and Country-by-Country Reports (CbCR), offering a detailed view of their global operations to tax authorities.

- This helps tax authorities identify potential discrepancies between profit allocation and actual business activities across jurisdictions.

- Transfer Pricing Adjustments

- The focus has shifted towards ensuring that intercompany transactions comply with the arm’s length principle, reflecting true market value.

- This requires companies to carefully document and justify pricing strategies used for intra-group transactions, minimizing audit risks.

- Risk of Penalties

- Non-compliance with BEPS guidelines can lead to tax adjustments, penalties, and reputational risks. Authorities now have more tools to detect profit shifting through the Automatic Exchange of Information (AEOI) framework.

- Substance Requirements

- Tax authorities scrutinize economic substance to ensure that MNEs cannot shift profits to low-tax jurisdictions without legitimate operational activities in those locations.

The adoption of BEPS guidelines has led to a stricter regulatory environment, and companies must align their tax strategies accordingly to mitigate risks. For more information on the BEPS initiative, refer to the OECD’s official BEPS policy page.

Changes to Financial Transactions Guidelines

In 2022, the OECD updated its Transfer Pricing Guidelines to provide clearer rules for the pricing of financial transactions between related parties. These changes address key areas such as intra-group loans, cash pooling, and financial guarantees, aiming to prevent profit shifting through the manipulation of financial transactions.

Key Changes and Their Implications

- Intra-Group Loans

- The new guidelines require companies to assess whether an intra-group loan is necessary and aligns with the arm’s length principle.

- Companies must consider the creditworthiness of the borrower and market conditions to ensure that loan terms reflect those that independent parties would offer.

- Cash Pooling Arrangements

- The guidelines provide detailed rules on centralized cash management practices within MNEs.

- They emphasize that the rewards from cash pooling must be allocated fairly, considering each participant’s contribution and risk exposure.

- Financial Guarantees

- The updated framework clarifies how financial guarantees between related entities should be priced, reflecting actual benefits received by the borrower.

- Mispricing such guarantees can lead to tax adjustments by authorities.

- Risk-Free and Risk-Adjusted Rates

- The guidelines introduce standards for determining risk-free and risk-adjusted returns, ensuring that returns on financial instruments align with market benchmarks.

These changes reinforce the importance of accurate documentation and benchmarking in financial transactions to comply with the OECD’s standards and prevent disputes. For further details, see the OECD’s 2022 Transfer Pricing Guidelines.

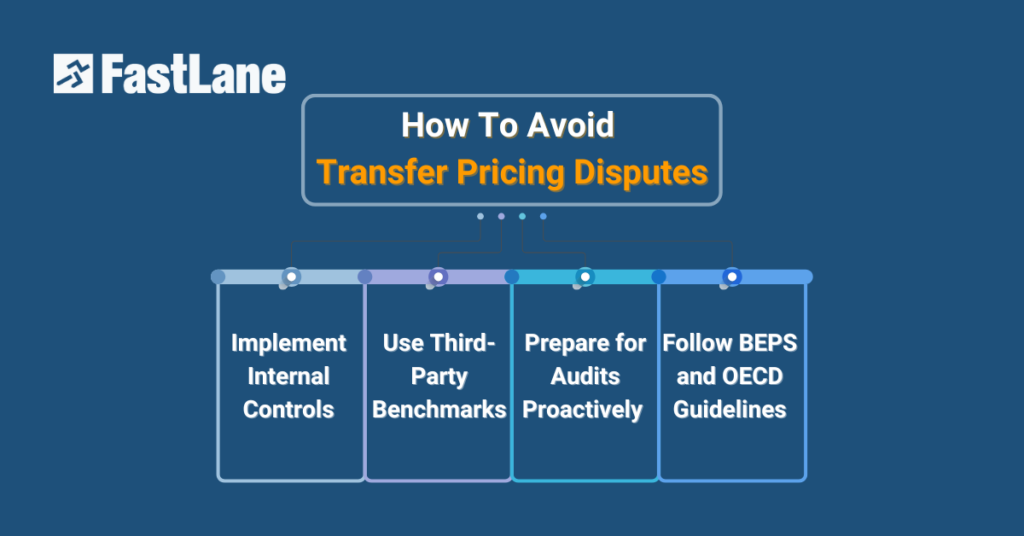

Best Practices to Avoid Transfer Pricing Disputes

- Managing Compliance Risks

Implement internal controls to regularly review intercompany pricing policies. Use third-party benchmarks to support transfer pricing positions.

- Preparing for a Transfer Pricing Audit

Maintain detailed records, including transfer pricing documentation and benchmarking studies and be ready to respond promptly to any IRD requests for information.

How to Optimize Your Tax Strategy with Transfer Pricing

Companies can leverage transfer pricing to optimize their tax liabilities. By ensuring that profits are allocated where value is created, businesses can align with global standards and reduce the risk of double taxation.

Global Disclosure Requirements And Hong Kong’s Transfer Pricing Framework

As part of the BEPS framework, Hong Kong requires increased transparency from MNEs through CbCR and documentation requirements. Compliance with these regulations helps companies avoid penalties and ensures smooth operations across borders.

Conclusion

Transfer pricing is essential for companies operating in Hong Kong with cross-border transactions. Adhering to IRD guidelines, maintaining proper documentation, and following best practices are crucial for compliance.

How FastLane Group Can Help with Transfer Pricing Compliance

FastLane Group offers specialized transfer pricing services, including documentation preparation, benchmarking studies, and audit support. Our team ensures that your business remains compliant with Hong Kong’s regulations while optimizing your tax strategy. Contact us to learn more about our transfer pricing services.

Frequently Asked Questions (FAQs) About Transfer Pricing

- What is transfer pricing documentation?

Transfer pricing documentation provides evidence that intercompany transactions align with the arm’s length principle. - Who must prepare the Master File and Local File?

Companies with significant revenue or related-party transactions are required to prepare these files. - What penalties apply for non-compliance?

The IRD may impose fines and conduct audits for companies failing to comply with transfer pricing rules.