Malaysia’s e-invoicing system has become a key component of modern business operations, designed to streamline transactions, improve compliance, and reduce paperwork in 2025. Under the guidelines of the Inland Revenue Board (IRB/LHDN), businesses are required to adopt electronic invoicing (e-invoices) for accurate reporting and real-time validation. To ease the transition, a 6-month relaxation period was introduced, allowing businesses flexibility in issuing consolidated and self-billed e-invoices. In this blog, we will explore the 5 main types of e-invoice in Malaysia including standard e-invoices, consolidated e-invoices, self-billed e-invoices, credit/debit/refund notes, and consolidated self-billed e-invoices—highlighting their features, usage, and compliance requirements for Malaysian businesses.

Key Summary

Types of e-invoice

Malaysia’s 2025 e-invoicing system introduces 5 e-Invoice types: standard, consolidated, self-billed, credit/debit/refund notes, and consolidated self-billed.

Standard e-invoice

e-Invoice ensures real-time validation with 55 mandatory fields for B2B and B2C transactions.

Consolidated e-Invoice

Consolidated e-Invoice simplifies B2C reporting by combining multiple transactions, but some industries are restricted.

Self-Billed e-Invoice

Self-Billed e-Invoice shifts responsibility to the buyer for specific scenarios like agent payments, foreign suppliers, and e-commerce.

Credit/Debit/Refund Notes

Credit/Debit/Refund Notes allow invoice adjustments, while Consolidated Self-Billed e-Invoices streamline high-volume buyer-issued transactions.

Relaxation Period

From 26 July 2024 to 31 Jan 2025, LHDN allowed flexibility for businesses to issue consolidated and self-billed e-Invoices before mandatory compliance began.

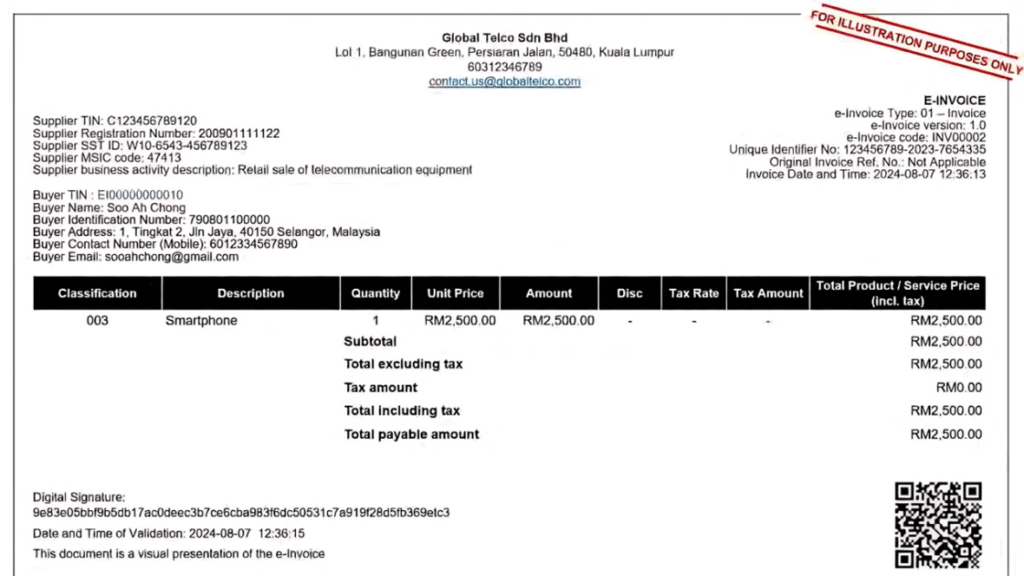

1. E-Invoice

An e-Invoice is the digital equivalent of a traditional paper invoice, serving as an electronic document that details the transaction between a buyer and a seller. Unlike physical invoices, e-Invoices are structured in a machine-readable format, allowing for faster processing and seamless compliance with Malaysia’s Inland Revenue Board (IRB/LHDN) requirements.

Key Features of an e-Invoice:

- Structured Data: Information is organized in a standardized format, making it easy for software and systems to read and process.

- Digital Format: Typically issued in XML or JSON, as mandated by the IRB.

- Mandatory Fields: Each e-Invoice requires 55 mandatory fields, with additional optional fields depending on transaction type. These cover supplier and buyer details, products or services, tax information, and payment data.

- Near Real-Time Validation: The IRB validates each e-Invoice and assigns a unique validation link for reference.

- Unique Identification: Every e-Invoice is given a distinct identifier by the IRB for tracking and compliance purposes.

- Security: Data is encrypted to ensure the confidentiality and integrity of sensitive financial information.

Learn: A Complete Guide To E-Invoice In Malaysia

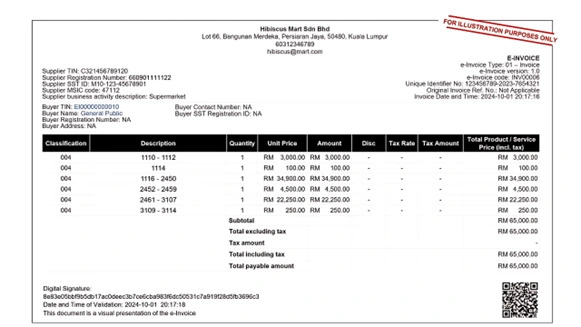

2. Consolidated e-Invoice

A Consolidated e-Invoice is an electronic document that merges multiple individual invoices, receipts, or transactions into a single e-Invoice. This approach is designed to simplify reporting and streamline invoicing, especially when a business issues multiple invoices to the same customer within a specific period (e.g., monthly). By combining transactions, suppliers reduce the need to issue separate e-Invoices for each transaction, making the process more efficient.

Applicability:

Consolidated e-Invoices are primarily used for business-to-consumer (B2C) transactions, where buyers do not require individual e-Invoices. Suppliers aggregate receipts or invoices and submit a consolidated e-Invoice as proof of income.

IRB Submission Timeline:

According to the Inland Revenue Board (IRB/LHDN) guidelines, suppliers must submit consolidated e-Invoices within 7 calendar days after the month-end.

Industries Prohibited from Issuing Consolidated e-Invoices:

Certain sectors are not allowed to issue consolidated e-Invoices and must issue individual e-Invoices for each transaction. These include:

- Automotive

- Aviation

- Luxury goods and jewelry

- Construction

- Wholesalers and retailers of construction materials

- Licensed betting and gaming

- Payments to agents, dealers, or distributors

Relaxation Period and Temporary Guidelines:

To ease the transition to e-invoicing, the IRB granted a 6-month relaxation period starting 26th July 2024, allowing businesses to issue consolidated e-Invoices for all transactions, including some that would normally require individual e-Invoices. This temporary measure provides businesses with flexibility to adjust to the new e-invoicing system before mandatory compliance.

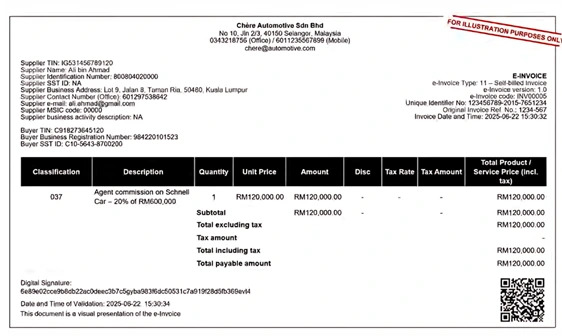

3. Self-Billed e-Invoice

A Self-Billed e-Invoice is an electronic invoice issued by the buyer instead of the seller, representing a deviation from the standard invoicing process. In this arrangement, the buyer assumes the responsibility of creating and submitting the invoice for a transaction, usually under specific circumstances as defined by the Inland Revenue Board (IRB/LHDN).

Scenarios Where Self-Billed e-Invoices Are Applicable:

Self-billed e-Invoices are commonly used in the following cases:

- Payments to agents, dealers, or distributors – when buyers manage commissions or fees directly.

- Goods or services from foreign suppliers – ensuring compliance and documentation for cross-border transactions.

- Profit distributions or financial allocations (e.g., co-operative or association payouts, not standard company dividends).

- E-commerce transactions – where platforms manage invoicing for multiple sellers.

- Payouts to betting and gaming winners – for regulatory and reporting accuracy.

- Acquisition of goods or services from individual taxpayers who are not conducting a business (only if other self-billed conditions do not apply).

- Interest, claims, or insurance payouts – with specific exclusions, e.g., business-charged interest to the public or foreign payors to Malaysian taxpayers.

Key Features of Self-Billed e-Invoices:

- The buyer is responsible for issuing, submitting, and validating the invoice via the MyInvois Portal.

- All mandatory e-Invoice fields, including supplier and buyer information, tax details, and transaction specifics, must be included.

- Ensures compliance and accurate reporting for transactions where the seller cannot issue the invoice.

4. Credit Note / Debit Note / Refund Note

In Malaysia’s e-invoicing system, adjustments to previously issued e-Invoices are managed through Credit Notes, Debit Notes, and Refund Notes. Each serves a distinct purpose for correcting or reconciling transactions.

Credit Note:

A credit note is issued by the seller to the buyer to reduce the amount owed. This usually occurs in situations such as:

- Returned goods or services.

- Pricing errors or discounts applied after invoicing.

- Damaged, defective, or incorrect items delivered.

A credit note references the original invoice, explains the reason for the credit, and indicates the adjusted amount, ensuring both parties maintain accurate financial records.

Debit Note:

A debit note serves the opposite purpose of a credit note, allowing the seller to add additional charges to a previously issued invoice. Common scenarios include:

- Extra items delivered or received.

- Undercharged prices or incorrect quantities.

Debit notes also reference the original invoice, specifying the reason and additional amount to be adjusted. They act as a formal document for financial reconciliation.

Refund Note:

A refund note confirms that the buyer will receive a return of money, usually due to:

- Defective, damaged, or incorrect goods.

- Cancelled orders or unfulfilled services.

- Services not rendered as agreed.

The refund note includes the original invoice number, reason for the refund, and the amount to be returned.

Error Handling and Adjustments via MyInvois Portal:

If an e-Invoice contains errors, the buyer can request a rejection, and the supplier may cancel the e-Invoice within 72 hours from the time of validation through the MyInvois Portal.

- If not rejected or cancelled within 72 hours, the e-Invoice is deemed valid and cannot be cancelled. Any later adjustments must instead be issued through a Credit Note, Debit Note, or Refund Note e-Invoice.

These adjustment documents are essential for accurate accounting, tax compliance, and smooth transaction management under Malaysia’s e-invoicing system.

5. Consolidated Self-Billed e-Invoice

A Consolidated Self-Billed e-Invoice is an electronic invoice that combines multiple self-billed invoices into a single document. Unlike standard self-billed e-Invoices issued individually by the buyer, this type of e-Invoice is designed to streamline high-volume transactions and simplify reporting.

Purpose:

This format is particularly useful in scenarios where buyers are responsible for issuing self-billed invoices for numerous transactions, such as:

- Insurance payouts to multiple individual policyholders.

- Interest or dividend payments to a large number of recipients.

- E-commerce or agent-based transactions with frequent, repeated invoicing.

By consolidating multiple self-billed invoices, businesses can reduce administrative workload and improve accuracy during validation.

Submission Timeline:

The consolidated self-billed e-Invoice must be submitted and validated via the MyInvois Portal within 7 calendar days after the month-end to comply with the Inland Revenue Board (IRB) regulations.

Relaxation Period Guidance:

During the 6-month relaxation period announced by LHDN on 26th July 2024, businesses were allowed to issue consolidated self-billed e-Invoices instead of individual self-billed invoices. This flexibility helps companies adjust to the e-invoicing system. Post-relaxation, from 1st February 2025 onward, Phase 1 taxpayers are required to issue individual self-billed e-Invoices for each transaction, except for transactions with individuals not conducting business, as specified under the guidelines.

Differences vs. Consolidated e-Invoice:

| Feature | Consolidated e-Invoice | Consolidated Self-Billed e-Invoice |

| Issuer | Supplier (seller) | Buyer |

| Purpose | Consolidate multiple sales for B2C transactions | Consolidate multiple self-billed transactions for specific scenarios |

| Usage Example | Retail store receipts | Interest or insurance payouts to individuals |

| Who Takes Invoicing Role | Seller | Buyer |

Learn: Latest E-Invoice Implementation Timeline in Malaysia

Key Differences Between e-Invoice Types

Understanding the differences between the various types of e-Invoices in Malaysia is crucial for compliance and efficient financial management. The table below summarizes the issuer, purpose, applicable scenarios, and examples for each type, including a clear comparison between Consolidated e-Invoice and Consolidated Self-Billed e-Invoice:

| Type of e-Invoice | Issuer | Purpose | Applicable Scenarios | Example |

| e-Invoice | Supplier | Standardized electronic invoice for transactions | All B2B or B2C transactions requiring near real-time validation | Regular sale of goods/services between businesses |

| Consolidated e-Invoice | Supplier | Combines multiple invoices/receipts into one document | B2C transactions where buyer does not require individual invoices | Retail store aggregating monthly customer receipts |

| Self-Billed e-Invoice | Buyer | Buyer issues invoice on behalf of supplier | Payments to agents, foreign suppliers, profit distribution, e-commerce transactions | Buyer paying multiple agents or distributors |

| Credit Note / Debit Note / Refund Note | Supplier | Adjustments or corrections to existing invoices | Returned goods, pricing errors, cancelled services | Issuing a credit note for returned defective goods |

| Consolidated Self-Billed e-Invoice | Buyer | Combines multiple self-billed invoices into one for streamlined reporting | High-volume self-billed transactions, e.g., payouts to individuals | Insurance company consolidating multiple claim payouts |

Key Comparison: Consolidated e-Invoice vs. Consolidated Self-Billed e-Invoice

| Feature | Consolidated e-Invoice | Consolidated Self-Billed e-Invoice |

| Issuer | Supplier | Buyer |

| Purpose | Consolidate multiple sales for reporting | Consolidate multiple self-billed transactions under specific scenarios |

| Applicable Scenarios | B2C transactions where buyer does not require individual e-Invoices | High-volume self-billed transactions like interest, insurance payouts |

| Example | Retail store receipts | Monthly insurance claim payouts to individuals |

| Invoicing Role | Seller | Buyer |

This clear distinction helps businesses select the correct e-Invoice type for each transaction, ensuring compliance with Malaysia’s Inland Revenue Board (LHDN) regulations and optimizing accounting workflows.

Learn: Malaysia E-Invoicing System: What Businesses Need to Know

Usage Guidelines For Different e-Invoice Types

To comply with Malaysia’s Inland Revenue Board (LHDN) regulations, businesses must choose the appropriate e-Invoice type based on transaction nature, volume, and invoicing responsibilities. Here’s a clear guide on when to use each type:

1. e-Invoice

- When to Use: For standard transactions between a buyer and a seller where full transaction details—including buyer, seller, goods/services, tax, and payment—must be electronically validated in near real-time.

- Tip: Always use e-Invoice for B2B transactions requiring immediate validation and compliance with IRB mandatory fields.

2. Consolidated e-Invoice

- When to Use: To combine multiple transactions or invoices (e.g., monthly) into a single document, especially for B2C transactions where buyers do not request individual e-Invoices.

- Tip: Ensure prohibited industries (automotive, aviation, luxury goods, construction, licensed betting, etc.) do not issue consolidated e-Invoices for restricted transactions.

3. Self-Billed e-Invoice

- When to Use: When the buyer is responsible for issuing invoices on behalf of the supplier, such as payments to agents, foreign suppliers, profit distribution, or e-commerce transactions.

- Tip: Ideal for scenarios where the buyer legally assumes the invoicing role; always confirm eligibility with LHDN guidelines.

4. Credit Note / Debit Note / Refund Note

- When to Use: For adjusting existing invoices due to returns, pricing errors, damaged goods, or service cancellations.

- Tip: Use these notes promptly within 72 hours of invoice validation for corrections, otherwise issue a new e-Invoice for adjustments.

5. Consolidated Self-Billed e-Invoice

- When to Use: To aggregate multiple self-billed invoices into a single document, commonly used for high-volume transactions such as insurance payouts, interest payments, or other self-billed scenarios.

- Tip: Submit and validate via the MyInvois Portal within 7 calendar days after month-end. During LHDN’s 6-month relaxation period, this type allows temporary flexibility for consolidated submissions.

Practical Tips for Businesses:

- Match e-Invoice Type with Transaction Role: Always check who is legally issuing the invoice—supplier or buyer.

- Check Industry Restrictions: Certain sectors cannot use consolidated e-Invoices; failure to comply may result in penalties.

- Use Consolidation Strategically: High-volume transactions can benefit from consolidated e-Invoices to reduce administrative burden, but avoid consolidation where individual validation is required.

- Stay Updated: LHDN periodically updates rules and relaxation periods; ensure your accounting system or e-invoicing software reflects the latest compliance requirements.

By following these guidelines, Malaysian businesses can streamline invoicing, maintain compliance, and reduce errors in their financial reporting while leveraging the benefits of e-invoicing.

Conclusion

Malaysia’s e-invoicing landscape has evolved significantly with the introduction of multiple e-Invoice types designed to streamline transactions, improve accuracy, and ensure compliance with LHDN regulations. From standard e-Invoices and self-billed e-Invoices to consolidated and credit/debit/refund notes, each type serves a specific purpose depending on transaction nature, volume, and who issues the invoice. By understanding the distinctions and proper usage guidelines for each e-Invoice type, businesses can reduce administrative burden, prevent errors, and maintain seamless regulatory compliance while benefiting from real-time validation and secure electronic processing.

How FastLane Group Can Help

Navigating Malaysia’s e-invoicing requirements can be complex, but FastLane Group provides expert support to simplify the process and ensure full compliance with LHDN/MyInvois standards.

Our Services Include:

- E-invoicing System Setup & Consultation: Tailored solutions to implement the right e-Invoice types for your business.

- Integration with Accounting Systems: Seamless connection between your invoicing software and ERP/accounting platforms for automated processing.

- Guidance on IRB/MyInvois Submissions: Expert assistance for accurate validation, submission, and compliance tracking.

With FastLane Group’s expertise, Malaysian businesses can focus on growth while we handle the complexities of e-invoicing compliance, ensuring accuracy, efficiency, and peace of mind. Contact us today!