If you have a business in Malaysia, it is important to understand the Sales and Services Tax (SST) system for better compliance and financial planning. This article will provide a simplified guide on what SST is, who has to pay SST and the requirements. Whether you are a new entrepreneur or want to ensure ongoing compliance, this guide will guide you everything you need to know about Malaysia’s SST framework.

Content Outline

Key Takeaways

SST is a Dual-Tax System in Malaysia

Malaysia’s Sales and Service Tax (SST) consists of Sales Tax on goods and Service Tax on specific services, applied at a single stage of the supply chain.

Different Rates Apply Based on Goods and Services

Sales Tax is charged at either 5% or 10%, while Service Tax is at 8%, with certain services like F&B, telecom, and logistics remaining at 6%.

Specific Goods and Entities Are Exempted

Goods essential to daily life, healthcare, and education are exempted from Sales Tax, along with approved manufacturers and public sector entities.

SST Registration Depends on Business Activity and Revenue

Businesses must register for SST if their taxable sales or services exceed RM 500,000 in the past 12 months, with special thresholds for some sectors.

Non-Compliance Can Lead to Heavy Penalties

Failure to file or pay SST on time can result in fines up to RM 50,000, imprisonment, or both so timely filling and payment is crucial.

What is Sales and Service Tax?

The Service Tax and Sales Tax (SST) in Malaysia is Malaysia’s primary consumption tax system, which comprises two elements: Service Tax and Sales Tax. SST is an introduction of a single-stage tax regime which is meant to be imposed at the manufacturing stage (for goods) or the point of delivery (for services). While the tax is paid by businesses, they pass on the burden to consumers through the final price of goods and services.

The Sales Tax is imposed on locally manufactured goods as well as imported goods, and is generally imposed at the manufacturing or importation stage.

The Service Tax is imposed on specific taxable services provided by registered businesses operating in Malaysia. These include the hospitality sector, professional services, telecommunications, and so on.

Sales and Service Tax Rates In Malaysia

Malaysia’s Sales and Service Tax (SST) framework consists of different tax rates depending on the nature of goods and services being sold.

Sales Tax Rates

Sales tax is imposed on taxable goods that are manufactured locally or imported into Malaysia. The applicable tax rates are as follows:

- 5% Sales Tax: Applied to a selected group of goods such as petroleum oils, construction materials, watches, and certain processed foodstuffs.

- 10% Sales Tax: This is the standard rate for most taxable goods, including luxury and non-essential items.

Service Tax Rates

Effective from 1 March 2024, Malaysia revised its service tax rates to better reflect the nature of services provided:

- 8% Service Tax: All taxable services are subject to this new rate, with the exception of the following categories listed below.

- 6% Service Tax: This lower rate continues to apply for food and beverage (F&B) services, telecommunication services, parking services, and logistics services, including newly covered logistics-related services.

To learn a complete list of taxable goods tax rates, read here.

Zero-Rated and Exempt Supplies

It is crucial to be able to distinguish between zero-rated and exempted goods or services:

- Zero-rated supplies are taxable but charged at 0%, typically to fund essential or export-oriented sectors.

- Exempted supplies are exempt from taxation and therefore not subject to SST at all.

What Goods Are Exempted From Sales Tax?

A variety of goods are exempted from Sales Tax to support essential needs, national development goals and export-driven industries. One of the key exemptions applies to goods manufactured specifically for export as the government aims to improve Malaysia’s global trade by relieving exporters from domestic tax burdens. Other sales tax-exempt goods include:

- Essential food items such as live animals, fish and seafood, meat, milk, eggs, vegetables, fruits and bread.

- Printed materials such as books, magazines, newspapers, journals and periodicals.

- Pharmaceutical and medical products such as multivitamin medicaments, medical cream, cough syrup, bandages etc.

- Fertilizers and pesticides including both animal-based and chemical types that are used in agriculture.

- Parts and accessories for bicycles that encourage environmentally friendly transportation.

- Precious metal items such as gold, platinum jewelry and silverware.

- Raw materials and chemicals used in the production of exempted goods.

The Sales Tax (Goods Exempted from Tax) Order 2018 listed the fill list of goods exempted from sales tax.

Who Is Exempted From Sales Tax?

As per Sales Tax (Person Exempted from Payment of Tax) Order 2018, certain individuals, organizations and manufacturers are granted exemptions based on the nature of their activities and public service roles.

Schedule A – Statutory and Government Entities

- Paramount Ruler (Yang di Pertuan Agong)

- State Rulers

- Federal or State Government Departments

- Local Authorities

- The Malaysian Armed Forces

- Importers for duty-free zones or shops

- Public higher education institutions

Schedule B – Approved Manufacturers

- Manufacturers approved by the Director-General of Customs for producing non-taxable goods.

- These businesses may be exempted from paying tax on materials, parts, packaging, and manufacturing aids used directly and solely in the production process

Schedule C – Manufacturers of Taxable Goods

- Registered manufacturers producing taxable goods may receive exemptions on the purchase of raw materials, components, packaging, and manufacturing aids, provided they are used solely in the manufacturing process

Who Needs To Pay SST in Malaysia?

In Malaysia, consumers are ultimately responsible for the Sales and Service Tax (SST) since it is included in the price of taxable goods and services. However, the responsibility to collect and remit SST to the Royal Malaysian Customs Department lies with taxable businesses especially, the manufacturers of taxable goods and service providers offering taxable services. These businesses are mandated to register for SST and act as intermediaries in collecting the tax on behalf of the authorities. In some cases, exempted businesses may do so voluntarily with the approval of the Director-General of Customs to maintain compliance or in the interest of business.

Which businesses must apply for sales and service tax registration in Malaysia?

In Malaysia, businesses that are involved in the supply of taxable goods or services are required to register for Sales and Service Tax (SST) if they meet the prescribed registration thresholds under the law. The requirements can be different based on whether a business is liable for Sales Tax or Service Tax.

Sales Tax Registration

Businesses must register for Sales Tax if they meet both of the following criteria:

- They are engaged in the manufacturing of taxable goods in Malaysia.

- Their total sales value of taxable goods in the past 12 months exceeds RM500,000.

Service Tax Registration

Businesses are required to register for Service Tax if:

- They provide taxable services as specified under the Service Tax Regulations.

- Their total value of taxable services in the preceding 12 months exceeds the applicable threshold.

Note: While the standard threshold is RM 500,000, it can different for certain industries and service categories.

| Service Tax Registration Thresholds by Business Type | |

| Taxable service provider | Registration Threshold |

| General taxable service providers (standard threshold) | RM 500,000 |

| Restaurants, bars, snack bars, food courts, etc. or any establishments offering food and beverage services for dining in or take-out. | RM 1.5 million |

| Credit/charge card providers regulated by Bank Negara Malaysia | No threshold |

| Approved customs agents offering specified customs-related services. | No threshold |

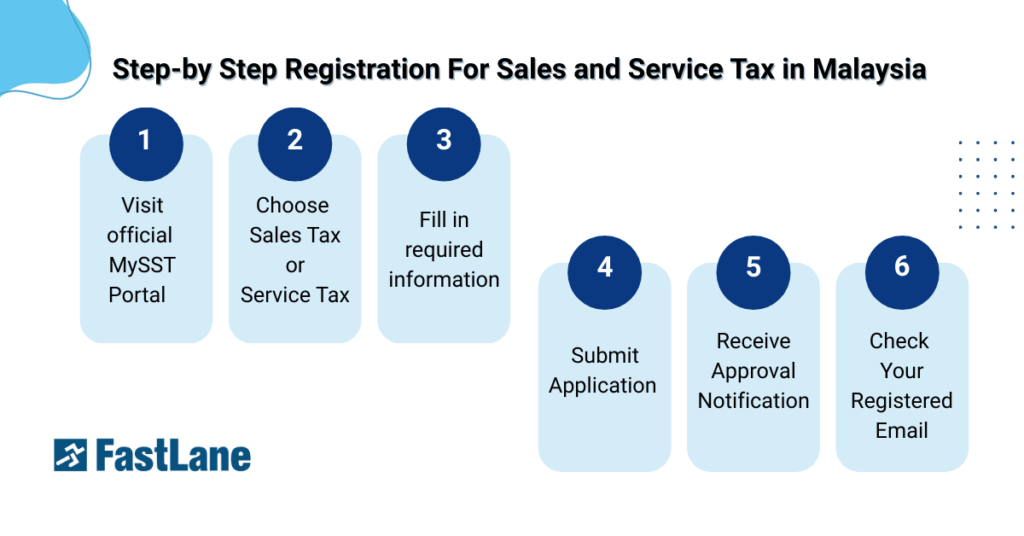

How to register for sales and service tax in Malaysia?

Registration for sales tax and service tax can be completed online. The registration for sales tax and service tax are separate, with their own process. Here is the step-by-step guide to help you register for SST in Malaysia.

- Visit official MySST Portal

- Choose whether you are registering for Sales Tax or Service Tax based on your business activity. Separate forms are used for each type.

- Fill in the required information accurately including:

- Business registration details (SSM/ROC?ROB)

- Business activity (manufacturing or service provision)

- Sales or service revenue figures

- Contact and business premises information

- Submit the Application

Review all entries for accuracy before submission. Once submitted, your application will be processed instantly through the MySST system.

- Receive Approval Notification

Upon successful registration, you will receive:

- A Sales Tax or Service Tax registration number

- An approval confirmation letter including your effective date of registration and applicable compliance obligations.

- Check Your Registered Email

A copy of the approval letter will be automatically sent to your registered email address for record-keeping and future reference.

Are foreign companies required to register for sales and service tax in Malaysia?

Foreign companies without a permanent establishment in Malaysia don’t need to register for sales tax or service tax.

When to file the sales and service tax return?

The filing period of the SST return is two months. If there is no tax to be paid, the return still must be filed. SST payment is due for receipt within 30 days of the end of the taxable period.

Applications for SST Malaysia can be submitted online via the CJP system or by downloading Form SST-02 from MySST and mailing it to the Customs Processing Centre (CPC).

The address is:

Jabatan Kastam Diraja Malaysia Pusat Pemprosesan Kastam Kompleks Kastam Kelana

Jaya No.22, Jalan SS6/3,

Kelana Jaya,

47301 Petaling Jaya,

Selangor

Penalties For SST Dues

Penalties are imposed on the following offences:

| Offence | Penalty |

| Failing to file the SST returns | A fine of up to RM 50,000A prison term up to three yearsOr both the fine and imprisonment. |

| Failing to make SST payment | A fine of RM 50,000A prison term up to three yearsOr both the fine and imprisonment |

| Late payment | Penalty rates charged is different depending on the durations of late payments: 1 – 30 days : 10%31-60 days: 15%61-90 days: 15%91 days and above : Maximum 40% |

Conclusion

Understanding and compliance with the Sales and Service Tax (SST) regime is essential for Malaysian companies. Whether manufacturing, rendering services, or both, keeping themselves updated on SST tax rates, exemptions, registration thresholds, and filing obligations helps the businesses avoid due penalties. With Malaysia continuing to simplify its tax code to more effectively address economic priorities, staying in compliance not only keeps you in line with the law but also secures your company’s reputation and budgeting.

Let FastLane Group simplify your tax journey. Whether you’re registering for SST, need help with tax filing, or looking for expert advisory, our team is here to support your business every step of the way. Contact us today for consultation!