If you have a business in Malaysia, it is important to understand the Sales and Services Tax (SST) system for better compliance and financial planning. This article provides a simplified yet comprehensive overview of Malaysia’s Sales and Service Tax (SST) system — what it is, who needs to comply, and key regulatory requirements. Whether you’re a new entrepreneur or an established business, this guide will equip you with everything you need to stay compliant under Malaysia’s SST framework.

What is Sales and Service Tax?

The Sales and Service Tax (SST) is Malaysia’s primary consumption tax system, comprising two main components: Sales Tax and Service Tax. SST is an introduction of a single-stage tax regime which is meant to be imposed at the manufacturing stage (for goods) or the point of delivery (for services). While the tax is paid by businesses, they pass on the burden to consumers through the final price of goods and services.

The Sales Tax is imposed on locally manufactured goods as well as imported goods, and is generally imposed at the manufacturing or importation stage.

The Service Tax is imposed on specific taxable services provided by registered businesses operating in Malaysia. These include the hospitality sector, professional services, telecommunications, and so on.

Sales Tax in Malaysia

Sales Tax in Malaysia is a single-stage tax imposed on taxable goods that are manufactured locally or imported into the country for domestic consumption. It is governed under the Sales Tax Act 2018 and administered by the Royal Malaysian Customs Department (RMCD).

All taxable goods produced or imported into Malaysia are subject to sales tax unless specifically exempted. Common exemptions include goods manufactured in or exported to free zones, licensed warehouses, Joint Development Areas (JDA), and the islands of Labuan, Langkawi, Tioman, and Pangkor.

Sales Tax Rates

Sales tax is levied at 5%, 10%, or a specific rate for petroleum products, depending on the category of goods and applicable tax schedule.

Registration Threshold

Businesses involved in manufacturing taxable goods with a total sales value exceeding RM500,000 within any 12-month period are required to register for sales tax with the RMCD. Voluntary registration is also allowed with Customs approval.

For importers, sales tax applies upon clearance of taxable goods at customs — however, no separate registration is required for importation activities.

What’s New for 2024–2025

Malaysia’s sales tax framework has undergone several key updates in 2025 to broaden tax coverage, enhance compliance, and align with global best practices.:

- 10% tax on Low-Value Goods (LVG): Effective 1 January 2024, imported goods valued at RM500 or below (sold online or imported by air, sea, or land) are now subject to a 10% sales tax.

- Expansion of taxable goods: More imported premium food items and construction materials are now included under the 5% rate, widening the tax net for businesses engaged in cross-border trade.

- Registration for LVG sellers: Overseas or local sellers with total sales of imported LVG exceeding RM500,000 over a 12-month period are required to register with RMCD as LVG-registered sellers.

Service Tax in Malaysia

Service Tax in Malaysia is a single-stage tax imposed on prescribed taxable services provided in the course or furtherance of business by a taxable person. This single-stage mechanism helps avoid tax-on-tax effects, simplifying compliance for service providers. It is governed under the Service Tax Act 2018 and administered by the Royal Malaysian Customs Department (RMCD).

This tax applies only once at the point of service provision, ensuring there is no double taxation along the supply chain.

Scope of Service Tax

Service tax applies to a wide range of prescribed services, including professional, consultancy, logistics, hospitality, food and beverage, telecommunications, and digital services. Businesses that provide these taxable services are required to charge and remit service tax once they exceed the registration threshold.

Since 1 January 2019, Malaysia’s service tax has also extended to imported taxable services — requiring both registered and non-registered businesses to self-account and remit tax on such services.

Service Tax Rates

The applicable rates depend on the category of service provided:

- 6% — applies to essential services such as food and beverage (F&B), telecommunications, logistics, and parking.

- 8% — applies to most other taxable services, including professional, management, and consultancy services.

Registration Thresholds

A business is required to register for service tax once its total taxable turnover exceeds the following thresholds within a 12-month period:

- RM500,000 — for most taxable services.

- RM1,000,000 — for rental and leasing services.

- RM1,500,000 — for construction and healthcare services.

Once the threshold is reached, the business must register with the RMCD and begin charging service tax on its taxable services to remain compliant.

2025 Updates — Expanded Coverage

Effective 2025, the Malaysian government has expanded the service tax scope to include:

- Private healthcare services provided to foreigners.

- Private education services offered to international students.

- Construction and renovation services for commercial and residential properties.

These updates reflect the government’s effort to broaden Malaysia’s service tax base while maintaining equitable tax treatment across industries.

In summary, Malaysia’s service tax framework continues to evolve, and businesses should regularly review their taxable activities to ensure compliance with the latest rates, thresholds, and scope expansions.

SST on Digital Services (SToDS)

The Service Tax on Digital Services (SToDS) was introduced on 1 January 2020 to ensure that foreign digital service providers contribute fairly to Malaysia’s tax system. This initiative aligns with global tax practices, addressing the growing digital economy and ensuring a level playing field for both local and foreign service providers.

Under the SToDS framework, an 8% Service Tax is imposed on digital services provided by foreign service providers (FSPs) to consumers—both individuals and businesses—in Malaysia.

Registration Requirement

Foreign providers are required to register for SToDS once their total value of digital services provided to Malaysian consumers exceeds RM500,000 within any 12-month period. The registration threshold can be determined using either:

- Historical method — based on actual revenue over the past 12 months, or

- Future method — based on projected revenue for the next 12 months.

Scope of Taxable Digital Services

Digital services refer to any services delivered over the internet or other electronic networks, which are automated and require minimal human intervention. Common examples include:

- Software-as-a-Service (SaaS) subscriptions

- Cloud storage and hosting services

- Online advertising and digital marketing platforms

- Streaming and entertainment services such as music or video platforms

Sales Tax Rates in Malaysia

Beginning 1 July 2025, Malaysia’s Sales Tax framework introduces revised rates aimed at distinguishing between basic necessities and non-essential or premium goods. This update ensures that essential daily items remain affordable while luxury and high-value products are taxed appropriately to enhance revenue fairness.

Sales Tax Rate Structure

| Category | Sales Tax Rate | Examples |

| Basic Necessities | 0% | Non-processed goods (chicken, fish, vegetables, local fruits), processed staples (flour, sugar, salt, cooking oil), medicines, books, journals, newspapers, fertilizer |

| Non-Essential Goods | 5% | Abalone, lobster, cheese, king crab, salmon, cod, truffle mushrooms, essential oils, silk |

| Premium and Luxury Goods | 10% | Shark fin, alcoholic drinks, leather goods, racing bicycles, antique hand paintings |

Key Highlights of the 2025 Sales Tax Revision

- Basic necessities remain zero-rated (0%), supporting affordability and food security.

- Non-essential and premium goods face increased tax rates, aligning with global consumption tax trends.

- Expansion of taxable goods now includes certain imported premium food items and luxury products under the 5% and 10% categories.

- Low-Value Goods (LVG) imported at or below RM500 continue to be taxed at 10%, ensuring fair treatment between local and international sellers.

Service Tax Rates

Effective 1 March 2024, the service tax rate in Malaysia has increased from 6% to 8%, along with an expanded scope of taxable services. This change affects a wide range of industries and professional services, while some categories remain at 6%.

| Group | Rate | Services Covered |

| A | 8% | Hotels, serviced apartments, bed & breakfasts |

| B | 6% | Restaurants, bars, coffee shops |

| C | 8% | Nightclubs, dance halls, cabarets, wellness centres, massage parloursProposed expansion: Karaoke centres |

| D | 8% | Private clubs including clubhouses based on membership, profession, or class |

| E | 8% | Golf courses or golf driving ranges |

| F | 8% | Betting, lottery, gambling machines or games of chance |

| G | 8% | Professional and management services: Legislation, accounting, assessment, engineering, architecture, consulting, training & coaching, IT/digital services, employment services, security/guard services, maintenance/repair (proposed), warehousing, parking, sports, secretarial services |

| H | 8% | Credit card services (RM25/year) |

| I | 8% | Insurance & takaful, telecommunications*, customs agents, vehicle parking providers*, motor vehicle services, courier services, rental and chauffeur services, advertising, domestic electricity >600 kWh, domestic travel (excluding RAS), cleaning, brokerage & guarantor services (proposed), real estate, ships/airplanes, commodities6% applies to F&B, telecommunication services, parking space providers |

| J | 6% | Logistics services including supply chain management, warehousing, freight forwarding, port/airport services, cargo transportation, e-commerce delivery, customs agents |

To learn a complete list of taxable goods tax rates, read here.

Expansion of Taxable Services (Effective 1 July 2025)

The Malaysian government expanded the Service Tax (SST) scope from 1 July 2025 to include several new service groups. These changes aim to align Malaysia’s tax framework with evolving industries such as wellness, healthcare, finance, and education.

| Taxable Service Group | Registration Threshold | Service Tax Rate | Who Will Be Affected |

| Group C – Wellness Centre | RM500,000 | 8% | Facial treatment providers, hair salons, barbershops, spas, and wellness centres offering massage, body treatments, slimming therapy, etc. |

| Group H – Finance | RM500,000 | 8% | Financial service providers earning income from fees, commissions, or similar payments (excluding basic banking, Syariah-compliant financing, and life insurance-related services). |

| Group I – Healthcare (for Non-Citizens) | RM1,500,000 | 6% | Private hospitals, clinics, and allied health professionals (e.g., physiotherapists, dietitians) serving foreign patients. |

| Group K – Rental or Leasing Services | RM500,000 | 8% | Landlords of commercial properties, machinery, or equipment leasing companies (excluding housing, reading materials, or assets outside Malaysia). |

| Group L – Construction Works | RM1,500,000 | 6% | Construction companies handling commercial or industrial buildings, contractors for infrastructure (roads, tunnels, bridges). |

| Group M – Education Services | NIL | 6% | Private schools charging above RM60,000 per student per year, universities and language centres offering courses to non-citizen students. |

Key Takeaway

From 1 July 2025, Malaysia’s expanded SST framework will bring more sectors under the tax net, including wellness, finance, healthcare, rental, construction, and education. Businesses in wellness, finance, healthcare, rental, construction, and education sectors should:

- Review their services and pricing models.

- Check if they meet SST registration thresholds.

- Prepare for invoicing and filing compliance under the new rules.

How to Calculate SST in Malaysia

Understanding how to calculate Sales and Service Tax (SST) correctly is essential for maintaining compliance and avoiding underpayment or overpayment. Below is a step-by-step guide that breaks down the formula, examples, and usage tips for Malaysian businesses.

SST Calculation Formula

The SST is calculated by applying the applicable tax rate to the taxable value of goods or services.

Sales Tax Formula

Sales Tax = Taxable Value of Goods × Applicable Sales Tax Rate (5% or 10%)

This formula applies to manufacturers, importers, or businesses selling taxable goods under the Malaysian Sales Tax regime. For inclusive pricing, businesses should use the back-calculation formula to separate the tax component from the final price.

Service Tax Formula

Service Tax = Value of Taxable Service × Applicable Service Tax Rate (6% or 8%)

This applies to service providers offering taxable services such as consulting, accounting, IT, F&B, or professional services.

Tip: Always confirm the correct rate for your goods or services through the Royal Malaysian Customs Department (RMCD) list of taxable items before applying SST.

SST Calculation Examples

Example 1: Service Tax

A consulting firm provides advisory services worth RM20,000.

The applicable Service Tax rate is 6%.

Service Tax = RM20,000 × 6% = RM1,200

Example 2: Sales Tax

A manufacturer sells taxable goods worth RM50,000 at a 10% Sales Tax rate.

Sales Tax = RM50,000 × 10% = RM5,000

In both cases, the tax is passed on to the end consumer, as SST is included in the final selling price of goods or services. Businesses act as tax collectors on behalf of the government.

Inclusive vs Exclusive SST — What’s the Difference?

Understanding whether SST is inclusive or exclusive of your total price is crucial for accurate invoicing and compliance.

- Inclusive — SST is already factored into the selling price.

- Exclusive — SST is added on top of the base price.

| Type | Example | Result |

| Inclusive of SST | Price = RM10,600 (includes 6% SST) | Tax = RM600; Net before SST = RM10,000 |

| Exclusive of SST | Price = RM10,000 (before SST) | Tax = RM600; Total with SST = RM10,600 |

3 Key Points to Calculate Your SST Threshold

Here are the three key points to help you calculate your SST threshold accurately.

Point 1. Which 12-Month Period Should You Look At?

SST registration is based on your total taxable revenue over any continuous 12-month period—not just your company’s financial year. This means you must regularly review your business revenue using one of the following scenarios:

| Scenario | Who It Applies To | How to Calculate |

| Scenario 1: Look at the Past 12 Months | For ongoing businesses | Review the current month and the previous 11 months of actual revenue (e.g. Aug 2024 – Jul 2025). |

| Scenario 2: Projected 12-Month Revenue | For newly operating businesses | Include the current month and the next 11 months of projected revenue (e.g. Aug 2025 – Jul 2026). |

| Scenario 3: Newly Established Company | For newly incorporated companies | Estimate annual revenue based on the first few months of operation (e.g. Jan – Aug 2025). |

Tip: Once your total revenue exceeds the threshold in any 12-month window, SST registration with the Royal Malaysian Customs Department (RMCD) becomes mandatory.

Point 2. Do Multiple Services Count Toward the SST Threshold?

Whether you offer a single service or multiple taxable services, it’s important to understand how your revenue is counted toward the SST threshold.

| Type of Service | Example | SST Registration Rule |

| Single Service | Construction service with RM1,500,000 revenue | Register — exceeded the RM1,500,000 threshold. |

| Multiple Services Within the Same Group | IT Service RM300,000 + Accounting Service RM300,000 → both under Group G | Combine revenue (RM600,000) — above RM500,000 threshold → registration required. |

| Multiple Services in Different Groups | IT Service (Group G) RM300,000 + Food & Beverage Service (Group K) RM300,000 | Evaluate separately — each group’s total below threshold → no registration needed. |

Tip: Even if some services are zero-rated or exempt, their revenue must still be considered when calculating your total taxable turnover within the same group.

Point 3. Are Different Branches or Subsidiaries Counted Separately?

If your business operates across multiple branches or entities, how you calculate SST thresholds depends on your legal structure:

| Business Structure | Example | How It Affects SST Threshold |

| Same Legal Entity (Same Sdn Bhd) | Branch A (RM300,000) + Branch B (RM300,000) = Accounting Sdn Bhd | Combine revenue — total RM600,000 → SST registration required. |

| Different Legal Entities (Different Sdn Bhds) | Branch A – Accounting Sdn Bhd (RM300,000), Branch B – Taxation Sdn Bhd (RM300,000) | Calculate separately — each entity below RM500,000 → no registration needed. |

Note: Even if both companies are related or share common ownership, SST thresholds are assessed based on legal registration, not business affiliation.

In Summary

- Always calculate revenue over a rolling 12-month period.

- Combine taxable services under the same SST group when determining thresholds.

- Add up all branch revenues under the same legal entity.

Understanding these rules helps ensure your business remains compliant with Malaysia’s updated SST regulations effective July 2025. If you need expert SST guidance, FastLane’s Malaysia tax specialists can help assess your SST eligibility, register your business, and streamline compliance.

What Goods Are Exempted From Sales Tax?

A variety of goods are exempted from Sales Tax to support essential needs, national development goals and export-driven industries. One of the key exemptions applies to goods manufactured specifically for export as the government aims to improve Malaysia’s global trade by relieving exporters from domestic tax burdens. Other sales tax-exempt goods include:

- Essential food items such as live animals, fish and seafood, meat, milk, eggs, vegetables, fruits and bread.

- Printed materials such as books, magazines, newspapers, journals and periodicals.

- Pharmaceutical and medical products such as multivitamin medicaments, medical cream, cough syrup, bandages etc.

- Fertilizers and pesticides including both animal-based and chemical types that are used in agriculture.

- Parts and accessories for bicycles that encourage environmentally friendly transportation.

- Precious metal items such as gold, platinum jewelry and silverware.

- Raw materials and chemicals used in the production of exempted goods.

The Sales Tax (Goods Exempted from Tax) Order 2018 lists the full set of goods exempted from Sales Tax.

Who Is Exempted From Sales Tax?

As per Sales Tax (Person Exempted from Payment of Tax) Order 2018, certain individuals, organizations and manufacturers are granted exemptions based on the nature of their activities and public service roles.

Schedule A – Statutory and Government Entities

- Paramount Ruler (Yang di Pertuan Agong)

- State Rulers

- Federal or State Government Departments

- Local Authorities

- The Malaysian Armed Forces

- Importers for duty-free zones or shops

- Public higher education institutions

Schedule B – Approved Manufacturers

- Manufacturers approved by the Director-General of Customs for producing non-taxable goods.

- These businesses may be exempted from paying tax on materials, parts, packaging, and manufacturing aids used directly and solely in the production process

Schedule C – Manufacturers of Taxable Goods

- Registered manufacturers producing taxable goods may receive exemptions on the purchase of raw materials, components, packaging, and manufacturing aids, provided they are used solely in the manufacturing process

Who Needs To Pay SST in Malaysia?

In Malaysia, consumers are ultimately responsible for the Sales and Service Tax (SST) since it is included in the price of taxable goods and services. However, the responsibility to collect and remit SST to the Royal Malaysian Customs Department lies with taxable businesses especially, the manufacturers of taxable goods and service providers offering taxable services. These businesses are mandated to register for SST and act as intermediaries in collecting the tax on behalf of the authorities. In some cases, exempted businesses may do so voluntarily with the approval of the Director-General of Customs to maintain compliance or in the interest of business.

Which businesses must apply for sales and service tax registration in Malaysia?

In Malaysia, businesses that are involved in the supply of taxable goods or services are required to register for Sales and Service Tax (SST) if they meet the prescribed registration thresholds under the law. The requirements can be different based on whether a business is liable for Sales Tax or Service Tax.

Sales Tax Registration

Businesses must register for Sales Tax if they meet both of the following criteria:

- They are engaged in the manufacturing of taxable goods in Malaysia.

- Their total sales value of taxable goods in the past 12 months exceeds RM500,000.

Service Tax Registration

Businesses must register for Service Tax if they provide prescribed taxable services and exceed certain thresholds:

- General threshold: Total taxable services exceeding RM500,000 in the past 12 months.

- Updated thresholds (effective July 2025):

- Rental/leasing and financial services: RM1 million

- Construction and private healthcare: RM1.5 million

- Private education: RM60,000 per student per year

Registration deadlines are tied to the date your business surpasses these thresholds. A grace period until 31 December 2025 allows new category businesses to register without penalties.

| Service Tax Registration Thresholds by Business Type | |

| Taxable service provider | Registration Threshold |

| General taxable service providers (standard threshold) | RM 500,000 |

| Restaurants, bars, snack bars, food courts, etc. or any establishments offering food and beverage services for dining in or take-out. | RM 1.5 million |

| Credit/charge card providers regulated by Bank Negara Malaysia | No threshold |

| Approved customs agents offering specified customs-related services. | No threshold |

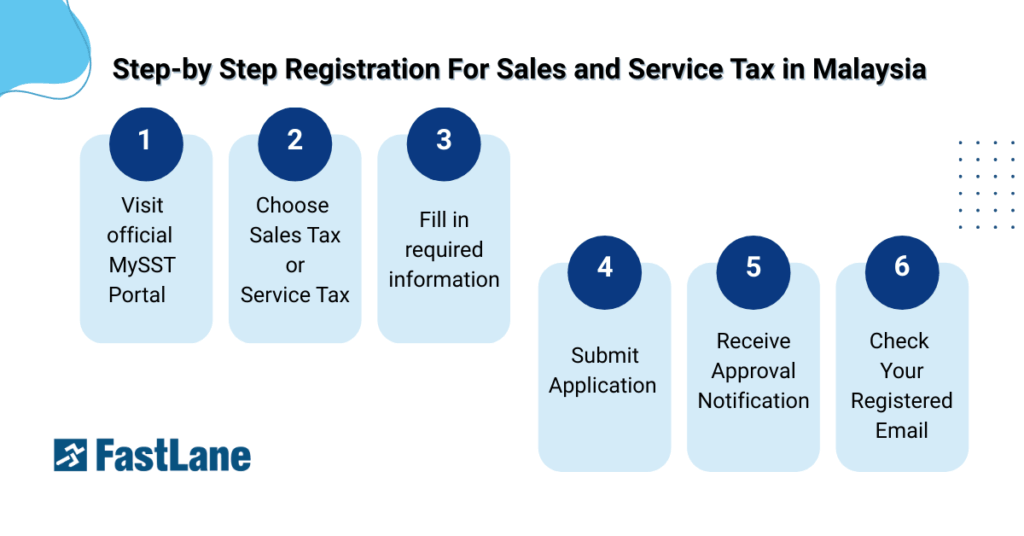

How to register for sales and service tax in Malaysia?

Registration for sales tax and service tax can be completed online. The registration for sales tax and service tax are separate, with their own process. Here is the step-by-step guide to help you register for SST in Malaysia.

- Visit official MySST Portal

- Choose whether you are registering for Sales Tax or Service Tax based on your business activity. Separate forms are used for each type.

- Fill in the required information accurately including:

- Business registration details (SSM/ROC?ROB)

- Business activity (manufacturing or service provision)

- Sales or service revenue figures

- Contact and business premises information

- Submit the Application

Review all entries for accuracy before submission. Once submitted, your application will be processed instantly through the MySST system.

- Receive Approval Notification

Upon successful registration, you will receive:

- A Sales Tax or Service Tax registration number

- An approval confirmation letter including your effective date of registration and applicable compliance obligations.

- Check Your Registered Email

A copy of the approval letter will be automatically sent to your registered email address for record-keeping and future reference.

Are foreign companies required to register for sales and service tax in Malaysia?

Foreign companies without a permanent establishment in Malaysia don’t need to register for sales tax or service tax.

When to file the sales and service tax return?

Filing SST returns is a mandatory requirement for all businesses registered under Malaysia’s Sales and Service Tax (SST) system. Every registered person must submit their SST declarations to the Royal Malaysian Customs Department (RMCD) within the prescribed filing period — even if no tax is payable for that period.

- Local Registered Businesses: SST returns must be filed every two months.

- Foreign Registered Persons (SToDS): Returns are filed every three months.

The SST payment must be received within 30 days after the end of the taxable period.

Timely and accurate filing helps businesses:

- Avoid late payment penalties and compliance risks.

- Maintain smooth financial operations and business continuity.

- Support effective cash flow and tax planning under Malaysia’s SST framework.

Tip: Even if your SST liability is zero, the return must still be filed within the due date to remain compliant with RMCD requirements.

Applications for SST Malaysia can be submitted online via the CJP system or by downloading Form SST-02 from MySST and mailing it to the Customs Processing Centre (CPC).

The address is:

Jabatan Kastam Diraja Malaysia Pusat Pemprosesan Kastam Kompleks Kastam Kelana

Jaya No.22, Jalan SS6/3,

Kelana Jaya,

47301 Petaling Jaya,

Selangor

Penalties For SST Dues

Penalties apply for failing to comply with SST filing or payment requirements. Updated rules include a grace period for late payments.

| Offence | Penalty |

| Failing to file SST returns | Fine up to RM50,000, or imprisonment up to 3 years, or both |

| Failing to make SST payment | Fine up to RM50,000, or imprisonment up to 3 years, or both |

| Late payment (updated) | Penalty rates vary by duration of delay: 1–30 days: 10% 31–60 days: 15% 61–90 days: 15% 91 days and above: Maximum 40% |

Note: A penalty-free grace period is in effect until 31 December 2025 for businesses making genuine efforts to comply with the new rules.

Key Considerations for Businesses

With Malaysia’s Sales and Service Tax (SST) framework continuing to evolve, it’s essential for both businesses and consumers to stay informed about the latest updates and regulatory changes. Keeping track of which goods and services are taxable and whether your business activities fall within the prescribed scope of SST helps ensure ongoing compliance and accurate tax reporting.

From time to time, the Royal Malaysian Customs Department (RMCD) may revise the scope of taxable items, exemptions, or available facilities, which could directly affect how businesses price their products and manage their tax obligations.

Once businesses have a clear understanding of these updates, they can incorporate them into their tax planning strategies to improve efficiency and reduce compliance risks.

Benefits of Effective SST Planning

Integrating SST considerations into your business planning offers several advantages:

- Better budgeting and financial forecasting through accurate tax estimation.

- Early identification of compliance gaps, allowing timely corrective action.

- Improved cash flow management by planning around SST payment cycles.

- Stronger operational efficiency by aligning internal processes with RMCD regulations.

Tip: Regularly review RMCD’s latest announcements and consult a professional to keep your SST strategy aligned with Malaysia’s evolving tax landscape.

Conclusion

Understanding and complying with Malaysia’s Sales and Service Tax (SST) regime is critical for every business. Staying updated with tax rates, exemptions, registration thresholds, and filing obligations helps companies avoid penalties, manage costs effectively, and maintain financial credibility. Whether manufacturing, rendering services, or both, keeping themselves updated on SST tax rates, exemptions, registration thresholds, and filing obligations helps the businesses avoid due penalties. With Malaysia continuing to simplify its tax code to more effectively address economic priorities, staying in compliance not only keeps you in line with the law but also secures your company’s reputation and budgeting. Let FastLane Group simplify your tax journey. Whether you’re registering for SST, need help with tax filing, or looking for expert advisory, our team is here to support your business every step of the way. Contact us today for consultation!