Dividend income refers to profits distributed by a company to its shareholders, usually in cash or additional shares. Since dividends are a common source of passive income, investors often ask whether this income is subject to tax in Hong Kong. The question is especially relevant for business owners, shareholders, and cross-border investors who want certainty around compliance and tax exposure. Hong Kong is known for its simple territorial tax system and generally favourable treatment of investment income, including dividends. In this blog, we explain how dividend income is treated under Hong Kong tax law, the types of dividends investors may receive, and the limited circumstances where additional review may be required.

Key Summary

Dividend Tax Treatment

Dividend income is generally not taxable in Hong Kong.

Territorial Tax System

Hong Kong taxes income based on source, not residency.

Foreign Dividends

Foreign-sourced dividends are generally not chargeable to Hong Kong tax, although foreign withholding tax may apply in the source country.

Limited Exceptions

FSIE rules may apply to certain foreign dividends received by multinational enterprise (MNE) entities.

Compliance Obligations

Companies must still record, disclose, and audit dividend income properly.

What Is Dividend Income?

Dividend income refers to the portion of a company’s profits distributed to its shareholders. When a company performs well and generates surplus earnings, it may choose to share these profits with its investors as dividends. By holding shares in a company, shareholders gain the right to receive these distributions based on the number of shares they own and the dividend amount declared.

Dividends are typically distributed either in cash or in the form of additional shares. Cash dividends are paid directly to shareholders through bank accounts or brokerage platforms, providing immediate income. Stock dividends, on the other hand, increase the shareholder’s equity in the company by issuing extra shares instead of cash. The method of distribution is determined by the company’s board of directors and its financial position.

In terms of timing, dividends are commonly paid on a regular schedule, such as quarterly or annually. Some companies may also declare dividends on an ad hoc basis, depending on profitability and business needs. Understanding how and when dividends are paid helps investors better assess expected income and plan their investment strategy, particularly in the context of Hong Kong’s tax treatment of dividend income.

Types of Dividend Income In Hong Kong

Dividend income in Hong Kong can be classified in several ways, depending on how dividends are paid and whether the distribution is part of a regular pattern. Understanding these differences helps investors assess cash flow, growth potential, and overall investment planning.

1. Cash Dividends vs. Stock Dividends

Cash dividends are the most common form of dividend income. They involve direct payments to shareholders, usually credited to a bank account or brokerage account. For investors seeking steady income, cash dividends provide immediate liquidity and predictable returns.

Stock dividends, in contrast, are issued as additional shares instead of cash. While there is no immediate cash payout, stock dividends increase the shareholder’s ownership in the company. This option is often more suitable for investors focused on long-term capital growth, as the value may increase if the company continues to perform well.

When choosing between cash and stock dividends, investors should consider whether their priority is short-term income or long-term value accumulation.

2. Regular Dividends vs. Special Dividends

Regular dividends are recurring distributions made as part of a company’s normal profit allocation. These payments are commonly issued on a quarterly or annual basis and are often used by investors to plan ongoing income and cash flow.

Special dividends are one-off payments declared under specific circumstances, such as exceptional profits, asset disposals, or corporate restructuring. Because they are not recurring, special dividends should not be relied on as a stable income source. Instead, they are best viewed as occasional returns linked to unique business events.

From a planning perspective, regular dividends offer greater predictability, while special dividends provide additional returns that may supplement an investor’s overall portfolio performance.

Read: Introduction to the Hong Kong Tax System

How Hong Kong’s Tax System Treats Dividends

Hong Kong’s favourable treatment of dividend income is closely linked to its tax framework. Understanding how the system works helps investors assess whether dividend income creates any local tax exposure.

Hong Kong’s Territorial Tax System Explained

Hong Kong operates under a territorial tax system. This means tax is generally charged only on income that is sourced in Hong Kong, such as profits arising from business activities carried on locally. Income that is offshore in nature is usually outside the scope of Hong Kong tax.

Because of this approach, most forms of passive investment income, including dividends, are not subject to tax in Hong Kong. Investors can hold shares in both local and overseas companies without triggering Hong Kong tax solely because they receive dividend payments. This framework is one of the key reasons Hong Kong remains attractive to regional and international investors.

Are Dividends Taxable in Hong Kong?

In general, dividend income is not taxable in Hong Kong. Dividends received by shareholders are typically not chargeable to salaries tax and are not included under personal assessment, so they generally do not form part of an individual’s net chargeable income for Hong Kong tax purposes.

This treatment applies broadly to both Hong Kong residents and non-residents, and it generally applies whether dividends are paid by a Hong Kong company or an overseas company. In most cases, shareholders can receive dividends in Hong Kong without additional Hong Kong tax.

For corporate recipients, foreign-sourced dividends may require review under Hong Kong’s Foreign-Sourced Income Exemption (FSIE) regime in certain circumstances (primarily for multinational enterprise (MNE) entities). Where FSIE is not relevant, dividend income remains generally non-taxable under Hong Kong’s territorial system.

Profit Tax and Dividends: How Double Taxation Is Avoided

One of the key strengths of Hong Kong’s tax system is that it avoids taxing the same income twice. This principle is especially important when it comes to profits tax and dividends.

Profit tax at the company level

In Hong Kong, companies are subject to profits tax on profits arising in or derived from Hong Kong. Before any dividends are paid, the company must first calculate its assessable profits and settle its profits tax liability with the Inland Revenue Department.

Only profits after tax can be distributed to shareholders. This means the income has already been taxed once at the corporate level, in line with Hong Kong’s territorial tax system.

Why dividends are not taxed again

To prevent double taxation, dividends paid out of taxed profits are generally not subject to further tax in Hong Kong. Dividend income is not included under salaries tax, personal assessment, or profits tax for the shareholder.

This treatment applies whether the shareholder is an individual or a company, and whether they are a Hong Kong resident or non-resident. As long as dividends are distributed from profits, they are generally not taxed again at shareholder level in Hong Kong.

This approach is a core reason why Hong Kong is attractive to investors and holding companies.

Practical explanation for shareholders

From a shareholder’s perspective, the process is straightforward.

- The company earns profits from its business activities.

- The company pays profits tax on those profits if they are Hong Kong sourced.

- The remaining after-tax profits are distributed as dividends.

- The shareholder receives the dividends without further Hong Kong tax liability.

In practical terms, shareholders do not need to declare dividend income in their personal tax returns, and companies generally do not pay tax again on dividends received from Hong Kong companies. This clear separation between corporate taxation and shareholder income helps reduce compliance complexity and supports efficient capital returns.

For businesses and investors alike, this system reinforces Hong Kong’s reputation as a low-tax, business-friendly jurisdiction.

Foreign Dividends and Withholding Tax

When investing in overseas companies, dividend income may be affected by tax rules outside Hong Kong. Understanding how foreign withholding tax works helps investors assess their actual after-tax returns.

What foreign withholding tax is

Foreign withholding tax is a tax imposed by the country where the dividend-paying company is located. Before the dividend is paid to a foreign shareholder, the company may be required to withhold a percentage of the dividend and remit it to the local tax authority.

The withholding tax rate depends on the source country’s domestic tax laws and any applicable double taxation agreement. As a result, investors may receive a net dividend amount after withholding tax is deducted overseas.

Why Hong Kong does not impose additional dividend tax

Hong Kong does not levy withholding tax on dividends, nor does it impose additional tax on foreign dividend income received by investors. This is consistent with Hong Kong’s territorial tax system, which focuses on taxing income sourced in Hong Kong rather than passive investment income.

As a general rule, foreign-sourced dividends are not chargeable to Hong Kong tax, subject to FSIE rules for certain MNE entities. Even when overseas withholding tax applies, Hong Kong does not tax the dividend again, which helps prevent double taxation at the investor level.

Importance of source-country rules

Although Hong Kong offers a favourable tax environment for dividend income, the tax treatment of foreign dividends is largely determined by the source country. Different jurisdictions apply different withholding tax rates, and some may offer reduced rates under double taxation agreements with Hong Kong.

Investors should review the dividend withholding rules of the country where the paying company is located and consider whether a tax treaty applies. This is especially important for cross-border investors and groups with overseas holdings, as the withholding tax can directly affect net investment returns.

Offshore Companies and Dividend Treatment

For companies structured to operate outside Hong Kong, dividend treatment is closely tied to the concept of offshore profits. Understanding how this works is critical for proper tax planning and ongoing compliance.

Meaning of offshore profits in Hong Kong

Under Hong Kong’s territorial tax system, profits are subject to profits tax only if they are sourced in Hong Kong. Offshore profits generally refer to income that is determined, based on the totality of facts test applied by the Inland Revenue Department, to be sourced outside Hong Kong.

In practice, the IRD examines where the profit-producing activities are carried out and where the relevant operations and key decision-making functions take place. The determination is made on a case-by-case basis, having regard to the overall facts and circumstances of the business.

When a company can substantiate that its profits are offshore in nature, those profits are generally not chargeable to Hong Kong profits tax. This principle applies regardless of where the company is incorporated, provided the source of profits is genuinely outside Hong Kong.

Dividend distributions from offshore profits

If a Hong Kong company earns offshore profits that are not subject to Hong Kong profits tax, dividends distributed from those offshore profits are also not taxable in Hong Kong. Shareholders receiving such dividends do not face salaries tax, personal assessment, or profits tax on the dividend income.

This treatment applies to both local and foreign shareholders. From a tax perspective, the key factor is the source of the underlying profits rather than the location of the shareholder or the place where dividends are paid.

Common compliance considerations

While offshore profits and related dividends may be non-taxable, companies must still meet strict compliance requirements. The Inland Revenue Department may request supporting documents to verify that profits are offshore sourced, including contracts, invoices, and operational records.

Companies are also required to maintain proper accounting records, file profits tax returns on time, and, where applicable, submit audited financial statements. Incorrect classification of profits or insufficient documentation can lead to disputes, additional tax assessments, and penalties.

For offshore structures, clear documentation and consistent operational practices are essential to support the non-taxable treatment of both profits and dividend distributions under Hong Kong tax rules.

Exceptions to Non-Taxable Dividends in Hong Kong

While dividends are generally not taxable in Hong Kong, there are limited situations where dividend income may require closer review. These exceptions are specific and mainly affect certain corporate structures rather than individual investors.

1. Foreign-Sourced Income Exemption (FSIE) Regime

Foreign-Sourced Income Exemption (FSIE) regime (effective 1 January 2023)

With effect from 1 January 2023, Hong Kong implemented refinements to the Foreign-Sourced Income Exemption (FSIE) regime to align its tax framework with international standards on base erosion and profit shifting.

Under the revised regime, certain categories of foreign-sourced passive income received in Hong Kong by specified entities may be regarded as chargeable to profits tax unless applicable exemption conditions are met. These categories include foreign-sourced dividends, interest, disposal gains, and income from intellectual property.

Impact on multinational enterprise (MNE) groups

The FSIE regime primarily targets multinational enterprise groups. Where an MNE entity receives foreign-sourced dividends in Hong Kong, those dividends may be taxable unless the entity can meet exemption conditions, such as economic substance requirements or participation exemptions.

These rules focus on corporate recipients within group structures rather than individual shareholders. As a result, dividend income received by group holding companies should be reviewed carefully to assess whether FSIE applies.

Why most individuals and SMEs are unaffected

For most individual investors and small to medium-sized enterprises, the FSIE regime does not change the practical tax position. Individuals receiving dividends from foreign or Hong Kong companies remain outside the scope of the FSIE rules.

Standalone local companies that are not part of an MNE group are also generally outside the scope of the FSIE regime.. In most cases, their dividend income continues to be treated as non-taxable in Hong Kong, provided there is no structured arrangement designed to shift profits.

2. When Dividend Income May Require Review

Although dividend income is usually exempt, certain situations warrant professional review to ensure compliance.

Group structures

Dividend income received within complex group structures may fall within the scope of FSIE. This is particularly relevant for holding companies receiving foreign dividends from overseas subsidiaries. The Inland Revenue Department may examine whether the income should be regarded as taxable under the revised rules.

Substance and economic presence considerations

For MNE entities, economic substance in Hong Kong has become increasingly important. Factors such as decision-making functions, employee presence, and operational activities may affect whether foreign-sourced dividends qualify for exemption.

Companies with limited substance in Hong Kong should assess their dividend flows carefully. Inadequate documentation or insufficient economic presence can increase the risk of tax challenges.

Double Taxation Agreements (DTAs) and Dividend Income

Hong Kong has built an extensive network of double taxation agreements to support cross-border investment and reduce unnecessary tax friction. These treaties play an important role in how foreign dividend income is taxed outside Hong Kong.

Purpose of Hong Kong’s tax treaties

Double taxation agreements are designed to prevent the same income from being taxed twice by different jurisdictions. For dividend income, DTAs clarify which country has the primary right to tax and how much tax can be imposed at source.

From a Hong Kong perspective, DTAs help provide certainty to investors and businesses investing overseas. They also support Hong Kong’s position as an international financial and holding company hub by reducing tax barriers on cross-border income flows.

How DTAs reduce foreign withholding tax

Many countries impose withholding tax on dividends paid to non-resident shareholders. Hong Kong’s DTAs often limit the maximum withholding tax rate that the source country can charge, provided specific conditions are met.

For example, reduced rates may apply where the Hong Kong recipient holds a minimum shareholding in the foreign company or meets qualifying company requirements under the relevant treaty. In some cases, the withholding tax on dividends may be reduced to a low rate or eliminated entirely.

These treaty benefits directly improve after-tax returns for Hong Kong investors but they depend on proper documentation, such as tax residency certificates, and compliance with the treaty conditions set by the source country.

DTAs do not create Hong Kong dividend tax obligations.

Double taxation agreements (DTAs) do not make dividends taxable in Hong Kong. Their purpose is to allocate taxing rights between jurisdictions and, where applicable, limit the amount of withholding tax that may be imposed by the source country.

Even where a DTA reduces foreign withholding tax, the dividend income generally remains not chargeable to Hong Kong tax under the territorial tax system. In practice, DTAs operate alongside Hong Kong’s dividend treatment to prevent double taxation, allowing investors to benefit from reduced foreign withholding tax while maintaining Hong Kong’s non-taxable treatment of dividends in most cases.

Read: A Guide To Double Taxation Agreement Hong Kong Tax Treaties

Dividend Withholding Tax Rates Under DTAs

Hong Kong does not impose withholding tax on dividends. However, when dividends are paid by overseas companies, foreign withholding tax may apply in the source country. Hong Kong’s double taxation agreements help reduce or cap this tax exposure and provide greater certainty for cross-border investors.

How treaty rates work in practice

Under a DTA, the source country agrees to limit the withholding tax rate on dividends paid to Hong Kong tax residents. Instead of applying its full domestic withholding tax rate, the source country applies the lower treaty rate, provided the recipient meets the qualifying conditions.

To benefit from a reduced rate, the Hong Kong recipient usually needs to demonstrate Hong Kong tax residency and satisfy the treaty requirements. This process is handled in the source jurisdiction and does not create any additional tax liability in Hong Kong. The dividend generally remains non-taxable under Hong Kong’s territorial tax system.

Shareholding thresholds and holding period requirements

Most DTAs include conditions that must be met before a reduced dividend withholding tax rate applies. These conditions vary by treaty but commonly include:

- A minimum shareholding percentage, often 10 percent, 15 percent, or 25 percent

- A minimum holding period, such as 12 months or 365 days

- Qualification as a company rather than an individual investor

If these thresholds are not met, the source country may apply its higher domestic withholding tax rate. Investors should review the relevant treaty carefully, as each agreement sets out its own conditions.

Why investors should review treaty eligibility

Treaty benefits are not automatic. Failure to meet the conditions or provide proper documentation can result in unnecessary withholding tax on dividend income.

For holding companies, group structures, and cross-border investors, reviewing treaty eligibility helps improve after-tax returns and reduce compliance risk. This is especially important where dividend amounts are significant or where shareholding structures have recently changed.

The table below is for general reference only; treaty application depends on facts, conditions, and documentation. Actual rates depend on the specific treaty terms and the investor’s circumstances.

Dividend Withholding Tax Rates Under Hong Kong DTAs

| Country | Dividends (Qualifying Companies) | Interest | Royalties |

| Armenia | 0% (holding ≥10% for 365 days) | Exempt (HK Gov entities) | NA |

| Austria | 0% (holding ≥10%) | Exempt (HK Gov entities) | NA |

| Bangladesh | 10% (holding ≥10%) | Exempt (HK Gov entities) | NA |

| Belarus | Exempt (HK Gov entities) | Exempt (HK Gov entities) | 3% (aircraft use) / 5% (others) |

| Belgium | 5% (holding ≥10%) / 0% (holding ≥25% for 12 months) | NA | NA |

| Brunei | NA | 5% (for banks) / 10% (others) | NA |

| Cambodia | NA | Exempt (for HK Gov entities) | NA |

| Canada | 5% (holding ≥10%) | NA | NA |

| Croatia | Exempt (for HK Gov entities) | Exempt (for HK Gov entities) | NA |

| Estonia | 0% (received by a company) | 0% (company) / 10% (others) | 0% (industrial use) / 3% (others) |

| Finland | 0% (holding ≥10%) | NA | NA |

| Georgia | Exempt (for HK Gov entities) | Exempt (for HK Gov entities) | NA |

| Hungary | 0% (holding ≥10%) | NA | NA |

| Indonesia | 5% (holding ≥25%) | NA | NA |

| Japan | 0% (holding ≥10%) | NA | NA |

| Korea | 5% (holding ≥25%) | NA | NA |

| Kuwait | 0% (if received by HK Gov entities) | NA | NA |

| Latvia | 0% (if received by a company) | 0% (if received by a company) / 10% (others) | 0% (industrial use) / 3% (others) |

| Luxembourg | 0% (holding ≥10%) | NA | NA |

| Malaysia | 0% (holding ≥10%) | NA | NA |

| Macao SAR | Exempt (for HK Gov entities) | Exempt (for HK Gov entities) | NA |

| Mainland China | 5% (holding ≥25%) | NA | 5% (aircraft or ship leasing) / 7% (others) |

| Mauritius | 0% (holding ≥10% for 365 days) | NA | NA |

| Mexico | NA | 4.9% (if received by a bank) / 10% (others) | NA |

| Netherlands | 0% (holding ≥10%) | NA | NA |

| New Zealand | 5% (holding ≥10%) / 0% (holding ≥50% and conditions met) | NA | NA |

| Pakistan | NA | Exempt (for HK Gov entities) | NA |

| Portugal | 0% (if holding ≥10%) | NA | NA |

| Romania | 5% (holding ≥15%) | 0% (if no interest tax) | NA |

| Russia | 5% (holding ≥15%) | NA | NA |

| Saudi Arabia | NA | NA | 5% (industrial use) / 8% (others) |

| Serbia | 5% (if holding ≥25% for 365 days) | NA | 5% (copyrights) / 10% (patents, trademarks, etc.) |

| South Africa | 0% (holding ≥10%) | NA | NA |

| Spain | 5% (holding ≥25%) | NA | NA |

| Switzerland | 0% (holding ≥10%) | NA | NA |

| Thailand | NA | 10% (for banks, insurance, business credit) / 15% (others) | 5% (copyrights) / 10% (patents) / 15% (others) |

| Türkiye | 5% (holding ≥25% for 365 days) | 7.5% (financial institutions, loan >2 years) / 10% (others) | 7.5% (industrial use) / 10% (others) |

| United Arab Emirates | 0% (if received by HK Gov entities) | NA | NA |

| United Kingdom | Exempt (except 15% on certain real estate vehicles) | Exempt (qualifying institutions) | NA |

| Vietnam | NA | NA | 7% (patents, designs) / 10% (others) |

How to Declare Dividend Income in Hong Kong

Dividend income is generally exempt from tax in Hong Kong. However, the reporting approach differs for companies and individuals. Understanding the correct declaration requirements helps avoid compliance issues and ensures accurate tax filings.

1. For Hong Kong Companies

Although dividends are usually non-taxable, Hong Kong companies still have reporting and documentation obligations under the profits tax framework.

Recording dividend income in financial statements

Hong Kong companies must record dividend income in their accounting records and financial statements in accordance with Hong Kong Financial Reporting Standards. This applies whether the dividends are received from local or overseas companies. Proper classification supports transparency and audit readiness, even when the income is exempt from tax.

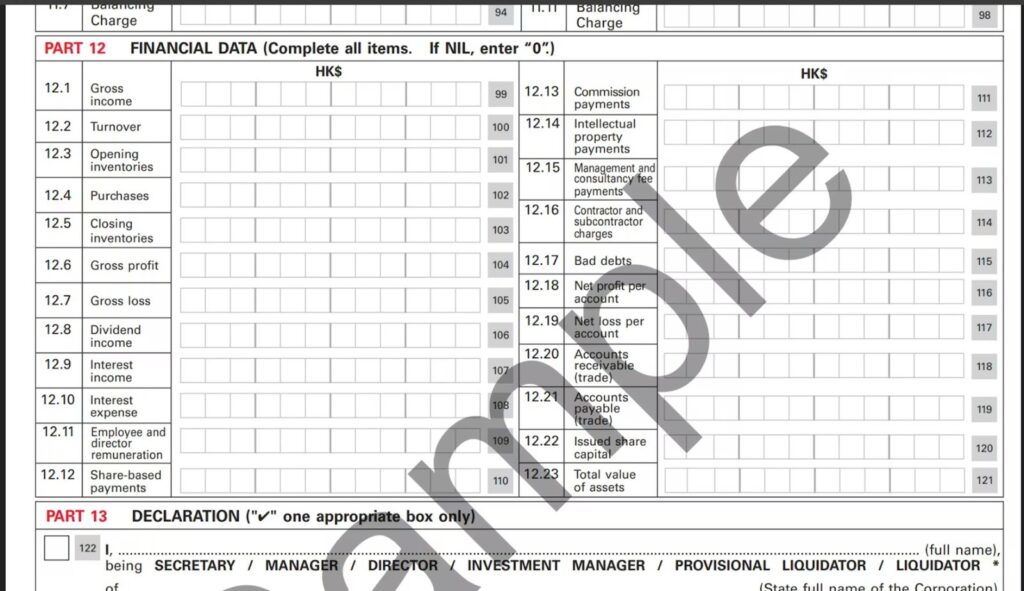

Profits Tax Return (BIR51) reporting

Dividend income must be disclosed in the Profits Tax Return. For BIR51 filers, dividends are reported in the Financial Data section, currently disclosed under Box 12.8 (subject to IRD form updates). The disclosure requirement applies even if the dividend income is not chargeable to profits tax.

Read: Hong Kong Tax Return Guide: Profits Tax Return (BIR51 / BIR52 / BIR54)

Audit and tax computation requirements

Hong Kong companies are required to submit audited financial statements together with their Profits Tax Return. A tax computation must also be prepared to reconcile accounting profit to assessable profits, clearly showing dividend income as non-taxable where applicable.

The tax computation should be prepared by a Hong Kong certified public accountant to ensure compliance with IRD requirements. Incomplete filings or incorrect disclosure may result in enquiries, delays, or penalties.

2. For Individuals

For most individual investors, dividend reporting is straightforward.

No declaration required for most dividends

Dividends received by individuals are generally not subject to salaries tax or personal assessment in Hong Kong. As a result, most individuals do not need to declare dividend income in their tax returns, unless the dividends are connected to a trade or business carried on in Hong Kong, regardless of whether the dividends are paid by Hong Kong or foreign companies.

This treatment applies to both Hong Kong residents and non-residents, provided the dividends are not connected to a trade or business carried on in Hong Kong.

Foreign withholding tax considerations

While Hong Kong does not tax dividends, foreign withholding tax may still apply when dividends are paid by overseas companies. Any withholding tax is imposed by the source country and is usually deducted before the dividend is paid.

Individuals should review the relevant double taxation agreement, if applicable, to understand whether a reduced withholding tax rate is available. However, foreign withholding tax does not need to be reported or claimed in Hong Kong, as the dividend itself remains exempt under Hong Kong tax rules.

Dividends vs. Capital Gains: Key Tax Differences

Dividends and capital gains are two common sources of investment returns. While both can increase overall wealth, Hong Kong’s tax treatment of each is different. Understanding these differences helps investors assess after-tax returns and structure investments more effectively.

1. Capital Gains Tax in Hong Kong

No capital gains tax in most cases

Hong Kong does not levy a standalone capital gains tax. In most situations, profits arising from the disposal of investments such as shares, bonds, or other securities are not taxable. This applies to both Hong Kong residents and non-residents.

For individual investors, gains made from buying and selling shares as long-term investments are generally regarded as capital in nature and fall outside the scope of profits tax.

Common exceptions

Capital gains may become taxable if the disposal is considered part of a trade or business carried on in Hong Kong. Common situations that may trigger tax exposure include:

- Frequent or systematic trading activities

- Short holding periods that indicate trading intent

- Disposal of assets as part of a business operation

- Gains arising from options or certain financial instruments

In these cases, the Inland Revenue Department may treat the gains as trading profits rather than capital gains, making them subject to profits tax. Each case is assessed based on its facts and circumstances.

2. Dividend Income Compared

Income versus disposal of investments

Dividend income arises from holding an investment, while capital gains arise from selling or disposing of an investment. In Hong Kong, dividends are generally not chargeable to Hong Kong tax under the territorial system, and Hong Kong does not impose a separate dividend withholding tax

This approach prevents double taxation and allows investors to receive dividend income without additional Hong Kong tax in most cases. Capital gains, when they are truly capital in nature, are also not taxed.

Why Hong Kong remains attractive to investors

The combination of no capital gains tax and exemption for most dividend income makes Hong Kong a highly attractive location for investors. Investors can focus on long-term value creation and income generation without significant local tax leakage.

When combined with Hong Kong’s territorial tax system and extensive network of double taxation agreements, this framework supports both local and cross-border investment strategies. For individuals and businesses seeking tax efficiency and regulatory certainty, Hong Kong continues to offer a favourable environment for building and managing investment portfolios.

Common Misunderstandings About Dividend Tax

Despite Hong Kong’s relatively simple tax framework, dividend taxation is often misunderstood. Clarifying these common misconceptions helps investors and businesses avoid unnecessary reporting errors and incorrect tax assumptions.

“Foreign dividends are taxable in Hong Kong”

This is one of the most common misunderstandings. In general, foreign-sourced dividends are not taxable in Hong Kong. Under Hong Kong’s territorial tax system, tax is charged only on income that is sourced in Hong Kong.

Dividends received from overseas companies are usually outside the scope of Hong Kong tax, regardless of whether the recipient is a Hong Kong resident. However, foreign withholding tax may still apply in the source country, depending on local laws and any applicable double taxation agreement.

There are limited exceptions, such as certain foreign dividends received by multinational enterprise groups under the Foreign-Sourced Income Exemption regime. These situations are specific and do not typically affect individual investors or standalone local companies.

“Dividends must be declared under salaries tax”

Dividends are not employment income and should not be reported under salaries tax. Salaries tax applies to income derived from employment, offices, or pensions, not to investment income.

Dividend income received by individuals is generally exempt from tax in Hong Kong and does not form part of net chargeable income. As a result, most individuals do not need to declare dividend income in their Salaries Tax Return.

“All offshore dividends are automatically non-taxable”

While most offshore dividends are not taxable in Hong Kong, they are not automatically exempt in every situation. The tax treatment depends on the nature of the recipient and the surrounding facts.

For example, dividends received by entities within a multinational enterprise group may be subject to additional conditions under the Foreign-Sourced Income Exemption rules. In these cases, economic substance and other requirements may need to be met for the income to remain non-taxable.

Investors and companies should review the source of dividends, the recipient’s structure, and any applicable tax rules to confirm the correct treatment. Seeking professional support helps ensure compliance while avoiding unnecessary tax exposure.

Practical Tips for Investors and Business Owners

While dividends are generally tax efficient in Hong Kong, proper management and compliance remain important. The following practical tips help investors and business owners reduce risk and stay aligned with Inland Revenue Department requirements.

Maintain Proper Dividend Records

Keep clear and complete records of all dividend income received. This includes dividend vouchers, bank statements, and shareholding documents. For companies, dividend income should be accurately recorded in the financial statements and reconciled with accounting records.

Proper documentation supports audit readiness and helps demonstrate the nature and source of dividend income if questions arise during tax reviews.

Understand Foreign Withholding Exposure

Although dividends are usually not taxable in Hong Kong, foreign withholding tax may apply in the country where the dividend-paying company is located. The withholding rate depends on local tax laws and any applicable double taxation agreement.

Investors should review dividend statements carefully and understand whether withholding tax has already been deducted. This helps avoid confusion over net returns and ensures accurate reporting where required.

Review FSIE Applicability for Group Structures

The Foreign-Sourced Income Exemption rules may affect certain foreign dividends received by entities within multinational enterprise groups. These rules are highly fact specific and focus on economic substance and holding arrangements.

Companies with overseas investments or group structures should periodically review FSIE applicability as structures or income flows change. Early assessment helps prevent unexpected tax exposure and supports proper structuring.

Ensure Timely and Accurate Tax Filing

For Hong Kong companies, dividend income must be correctly reflected in audited financial statements and reported in the Profits Tax Return. Tax computations should be prepared carefully to ensure consistency with accounting records.

Timely and accurate filing reduces the risk of penalties and follow-up enquiries from the Inland Revenue Department. Engaging professional support can help businesses meet compliance obligations while maintaining tax efficiency.

Why Hong Kong Is Attractive for Dividend Investors

Hong Kong’s tax framework is one of the key reasons it remains a preferred jurisdiction for dividend-focused investors. Its simple rules and investor-friendly policies provide clarity and long-term confidence for both individuals and businesses.

No Dividend Tax

Dividends received by shareholders are generally not subject to tax in Hong Kong. This applies to dividends from local companies as well as most foreign companies. Since dividends are not included in salaries tax or personal assessment, investors can retain the full amount received, subject only to any foreign withholding tax imposed by the source country.

No Capital Gains Tax

Hong Kong does not levy capital gains tax on the sale of investments such as shares. This means investors can benefit from both regular dividend income and investment appreciation without additional tax exposure. For long-term investors, this significantly enhances overall returns.

Clear and Predictable Tax System

Hong Kong operates under a territorial tax system, taxing only income sourced in Hong Kong. The treatment of dividends is well established and consistently applied, reducing uncertainty for investors. Clear guidance from the Inland Revenue Department also makes compliance more straightforward.

Extensive Tax Treaty Network

Hong Kong has an expanding network of comprehensive double taxation agreements with major economies. These treaties can help reduce foreign withholding tax on dividends and improve cross-border investment efficiency. For investors holding overseas assets, this adds an extra layer of tax certainty and planning flexibility.

Conclusion

Hong Kong’s dividend tax regime remains highly attractive for investors and business owners. Dividends received by shareholders are generally not taxable, and there is no capital gains tax on investment disposals, provided the income falls outside specific exception regimes such as the FSIE rules for certain multinational group structures. Despite this favourable treatment, proper reporting and compliance are still critical. Companies must ensure dividend income is accurately recorded in their financial statements, correctly disclosed in Profits Tax Returns, and supported by audited accounts to reduce compliance risks and avoid IRD enquiries.

How FastLane Group Can Help

FastLane Group supports businesses with accounting, audit coordination, and profits tax filing relating to dividend income in Hong Kong. Our experienced team helps ensure accuracy, consistency, and timely filing in line with IRD requirements.

- Accounting and bookkeeping support to properly record dividend income and maintain compliant financial records

- Audit arrangement and compliance support with Hong Kong certified public accountants to meet statutory audit requirements

- Profits tax filing services to prepare and submit accurate Profits Tax Returns with appropriate disclosures

If you need professional support with accounting, audit arrangement, or profits tax filing in Hong Kong, contact us to manage your compliance obligations with confidence and clarity.