In Hong Kong, a current account is the cornerstone of both personal and business banking. For individuals, it serves as the central hub for receiving salaries, paying bills, and managing everyday spending. For businesses, a current account is a necessity which enables smooth operations, payroll management, supplier payments, and regulatory compliance. With Hong Kong’s reputation as an international financial centre, current accounts play a vital role in ensuring seamless cash flow and supporting both local residents and global companies that choose the city as their business base.

Key Takeaways

Definition & Purpose

A current account in Hong Kong is designed for daily transactions, making it essential for both individuals and businesses to manage salaries, bills, payroll, and supplier payments.

Current vs Savings

Unlike savings accounts, current accounts prioritise flexibility and frequent transactions over interest earnings, supporting smoother cash flow.

Types of Accounts

Options include personal, business, multi-currency, and premium current accounts, each tailored to specific financial needs.

Fees & Requirements

Local banks often impose minimum balance rules and service fees, while virtual banks offer low-cost, app-based alternatives for startups and individuals.

Business Advantage

A well-managed current account strengthens cash flow, simplifies compliance, reduces FX costs, and builds credibility with investors and partners.

What Is A Current Account?

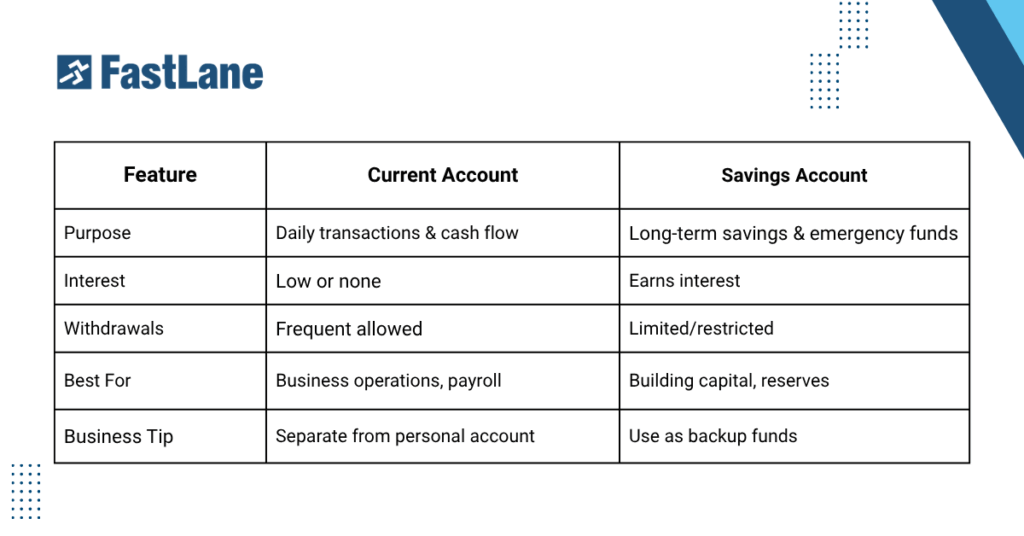

A current account is a type of bank account designed for day-to-day financial transactions which makes them one of the most essential tools for both individuals and businesses in Hong Kong. Unlike savings accounts, which focus on growing deposits through interest, a current account prioritises accessibility and flexibility allowing you to manage cash flow, pay expenses, and receive funds efficiently.

For individuals, a current account is commonly used to receive salaries, pay bills, and make everyday purchases using debit cards, cheques, or online transfers. For businesses, it serves as the backbone of operations, enabling payroll management, supplier payments, and multi-currency transactions that are critical in Hong Kong’s role as an international financial hub.

The main distinction between a current account and a savings account lies in their purpose:

- Current account → transactional, designed for frequent deposits and withdrawals.

- Savings account → interest-bearing, designed to help accumulate funds over time.

A current account in Hong Kong acts as your primary operating account that offers the convenience and financial control needed to manage both personal and business activities in a fast-paced economy.

Current Account vs Savings Account in Hong Kong

When managing finances in Hong Kong, it’s crucial to understand the difference between a current account and a savings account, especially for businesses.

Savings Accounts: For Wealth Accumulation

Savings accounts are primarily designed for storing funds over the long term while earning interest. They often have restrictions on the number of withdrawals to encourage saving, and some fixed-term savings options further limit access to funds. This makes them ideal for building capital or emergency reserves, rather than handling frequent transactions.

Current Accounts: For Daily Transactions

Current accounts, on the other hand, are tailored for day-to-day financial activities. They support frequent deposits and withdrawals, direct debits, standing orders, and international transfers. This flexibility makes them the preferred choice for operational expenses, payroll management, and handling cash flow in businesses.

Why Businesses Should Separate Personal and Company Accounts

For entrepreneurs and companies in Hong Kong, maintaining separate current accounts for personal and business finances is essential. A dedicated business account ensures accurate bookkeeping, simplifies tax reporting, and improves credibility with banks, investors, and suppliers. Mixing personal and business transactions in a single account can lead to accounting errors, compliance issues, and even potential legal complications.

By understanding the distinct purposes of current and savings accounts, businesses can optimize financial management, safeguard funds, and ensure smooth day-to-day operations in Hong Kong’s dynamic business environment.

Are Current Accounts Free in Hong Kong?

Current accounts in Hong Kong are not always free and understanding the fee structures is key to managing your banking costs effectively. While some basic accounts may come with minimal charges, most banks apply monthly maintenance fees, minimum balance requirements, or transaction-related costs.

Fee Structures to Expect

- Monthly service fees – Many traditional banks charge HKD 100–200 per month if your balance falls below the required minimum.

- Minimum balance requirements – Local banks often require anywhere between HKD 5,000 to HKD 50,000 as a minimum average balance. Falling short can trigger monthly fees.

- Transaction fees – Outgoing telegraphic transfers, cheque issuance, and cross-border payments may carry additional charges.

Local Banks vs. Virtual Banks

- Local banks (HSBC, BOC, DBS) – These institutions provide a wide range of current account services, but usually come with higher minimum balance thresholds and service fees. They are suitable for businesses and individuals who require in-branch support, multi-currency accounts, and access to international banking networks.

- Virtual banks (ZA Bank, WeLab Bank, Ant Bank) – Licensed digital-only banks offer current accounts with no minimum balance requirements and zero monthly fees, making them attractive for startups, freelancers, and individuals who prefer app-based banking. However, their services may be more limited compared to traditional banks, especially for corporate clients.

Tips to Avoid Unnecessary Fees

- Maintain the minimum balance required by your bank to waive service charges.

- Use online banking and mobile apps to reduce transaction fees tied to in-branch services.

- For SMEs and startups, consider virtual banks that offer no-fee current accounts with fast account opening.

- Compare bank packages regularly. Some institutions offer fee waivers for new customers or bundled business services.

For businesses in Hong Kong, choosing between a traditional bank and a virtual bank depends on your needs. If you rely on multi-currency trade and require a strong international network, a traditional bank may be worth the higher fees. If your focus is cost-efficiency and digital convenience, a virtual bank could be the smarter choice.

Types of Current Accounts In Hong Kong

Hong Kong banks provide different types of current accounts to serve the city’s diverse financial needs from individuals and expats managing daily expenses to multinational businesses handling global transactions. Choosing the right account type depends on your financial goals, business structure, and lifestyle.

1. Personal Current Accounts

These are designed for individuals, including local residents and expats. A personal current account allows you to receive salaries, pay bills, and manage everyday spending through debit cards, cheques, and online transfers. For expats, many banks provide multi-currency features and international transfer options to make managing finances between Hong Kong and overseas easier.

2. Business Current Accounts

For companies registered in Hong Kong, a business current account is mandatory for operations and tax compliance. Businesses use these accounts to handle payroll, supplier payments, invoicing, and government tax submissions. Most banks offer packages that include corporate internet banking, merchant services, and multi-user access to support SMEs, startups, and larger enterprises.

3. Multi-Currency Current Accounts

As an international finance hub, Hong Kong is home to businesses that trade across borders. Multi-currency current accounts allow account holders to hold, receive, and send funds in major currencies like USD, EUR, GBP, RMB, and JPY. This is especially valuable for import/export businesses, e-commerce companies, and global service providers, helping reduce foreign exchange costs and simplify international transactions.

4. Premium or Packaged Current Accounts

High-net-worth individuals and established businesses may choose premium or packaged accounts for value-added benefits, such as dedicated relationship managers, preferential FX rates, investment-linked services, and higher transaction limits. While these accounts often require maintaining a high minimum balance, they provide personalised services that go beyond standard banking.

If you’re an entrepreneur in Hong Kong trading internationally, combining a business current account with a multi-currency feature can streamline both local compliance and global transactions.

How To Open a Current Account In Hong Kong

Opening a current account in Hong Kong is an essential step for both individuals and businesses looking to manage finances efficiently in one of the world’s top financial hubs. While the process is straightforward, Hong Kong banks apply stringent compliance checks to meet global anti-money laundering (AML) and Know-Your-Customer (KYC) standards.

Eligibility

- Hong Kong residents – individuals with valid Hong Kong Identity Cards.

- Expats – foreign nationals living in Hong Kong, subject to additional documentation.

- Companies – both local entities and foreign-registered businesses operating in or through Hong Kong.

Requirements

- For individuals:

- Valid passport or Hong Kong Identity Card

- Proof of residential address (e.g., utility bill, tenancy agreement, bank statement)

- For businesses:

- Certificate of Incorporation and Business Registration Certificate

- Articles of Association

- Identification documents of directors and shareholders

- Proof of business operations (e.g., invoices, contracts, or website)

Application Process

- Submit application – online or at a branch, depending on the bank.

- KYC & compliance review – banks conduct detailed background checks to verify your identity and business activities.

- Bank interview – some banks may require a face-to-face or video interview, especially for corporate accounts.

- Approval & account setup – once approved, you receive account details, cheque books, debit cards, and access to online banking.

Learn more: How To Open A Bank Account In Hong Kong 2025

Challenges for SMEs & Startups

Opening a business current account can be particularly challenging due to:

- Stringent compliance – startups without a proven track record may face extra scrutiny.

- Minimum deposit requirements – some banks require a significant initial deposit or ongoing balance.

- Lengthy processing times – account approval may take weeks, especially for overseas-owned entities.

Tip: SMEs and startups often benefit from working with professional service providers who can help prepare the necessary documentation, strengthen compliance profiles, and connect with banks that are more open to new businesses.

How To Manage Your Current Account Effectively

Having a current account in Hong Kong is only the first step. Effectively managing your account ensures you avoid unnecessary fees, maintain healthy cash flow, and maximise the benefits of your account. With Hong Kong’s advanced banking system and digital tools, you can stay in full control of your finances if you adopt the right practices.

1. Monitoring Account Balance

Regularly checking your account balance helps you stay on top of spending and prevents costly overdrafts. Most Hong Kong banks provide mobile apps and online banking platforms with features like:

- Low-balance alerts to warn you before you go negative

- Instant transaction notifications for real-time updates

- Digital statements for easy tracking of monthly cash flow

2. Direct Debits & Standing Orders

Automating payments is a smart way to manage recurring obligations in Hong Kong.

- Direct debits for paying rent, utilities, or insurance premiums automatically.

- Standing orders for fixed payments like staff salaries or supplier contracts.

These features reduce the risk of late payments and ensure your financial commitments are always met on time.

3. Using Mobile & Online Banking Tools

Hong Kong’s banks are known for their cutting-edge digital platforms, making financial management simple and efficient. Mobile and online banking tools allow you

- To access accounts anytime, anywhere, manage multi-currency balances (HKD, USD, RMB, EUR, etc.),

- Transfer funds instantly within Hong Kong via Faster Payment System (FPS),

- Track your spending through categorised expense reports.

For SMEs and frequent international traders, multi-currency features are particularly valuable in reducing FX conversion costs.

4. Understanding Overdraft Options

An overdraft can act as a short-term financial buffer, but it needs to be managed wisely:

- Arranged overdraft: A pre-agreed facility with your bank, usually with lower fees and interest.

- Unarranged overdraft: It happens when you spend beyond your balance without prior approval which often results in hefty charges and negative impact on your credit record.

If you rely on overdraft facilities, always choose for an arranged limit and monitor your usage carefully to avoid unnecessary costs.

By combining regular monitoring, automation, and smart use of digital tools, you can manage your current account in Hong Kong effectively, safeguard your financial health, and support both personal and business growth.

Current Account & Business Growth in Hong Kong

In Hong Kong’s fast-paced financial hub, a current account is a foundation for business growth and sustainability. Managing your account effectively supports funding opportunities, payroll obligations, and international trade, all of which are critical to staying competitive.

Investor Funding and Capital Injection

For startups and SMEs, a current account provides the official channel for receiving investor funds or capital injections. Venture capital firms and angel investors in Hong Kong often require businesses to hold a corporate current account for transparency and compliance, ensuring that funding is traceable and properly managed.

Payroll Management

Whether you’re running a small team or a regional office, payroll efficiency depends on a reliable current account. Automating salary disbursements through standing orders or direct debits not only saves time but also builds employee trust by ensuring payments are made on schedule.

International Trade and FX Handling

As a leading international trade hub, Hong Kong businesses rely heavily on current accounts with multi-currency capabilities. These accounts simplify foreign exchange (FX) management, reduce conversion costs, and streamline cross-border payments. Having instant access to multi-currency balances helps companies manage trade receivables and pay overseas suppliers without delays.

Cash Flow Management: Deficit vs. Surplus

Just as economies face deficits and surpluses, businesses encounter similar challenges with cash flow.

- A cash flow deficit occurs when outflows (e.g., supplier payments, payroll, rent) exceed inflows, risking overdrafts and reliance on costly short-term financing.

- A cash flow surplus reflects healthy operations, where revenues and capital inflows exceed expenses, allowing businesses to reinvest, expand, or build reserves.

Regular monitoring of your current account balance with digital banking alerts and transaction tracking ensures you can anticipate shortfalls, maintain positive cash flow, and plan for growth.

Tip: Treat your business current account like a financial dashboard. By maintaining a surplus, you strengthen investor confidence, improve creditworthiness, and position your company for sustainable expansion in Hong Kong’s competitive market.

Learn more: 10 Best Payment Gateways For Hong Kong Businesses In 2025

Special Considerations For Current Accounts in Hong Kong

While a current account is essential for managing day-to-day transactions, there are several important factors to consider in Hong Kong’s financial landscape:

1. Exchange Rates for International Transactions

Hong Kong is a global trading hub, and many businesses and individuals rely on current accounts for cross-border transfers and foreign currency settlements. Exchange rate fluctuations can significantly impact the value of your international transactions. For businesses, this may affect profit margins when paying suppliers or receiving overseas payments. Choosing a current account that offers multi-currency support and competitive FX rates can help reduce costs and protect against currency volatility.

2. Credit History and Account Opening Eligibility

Banks in Hong Kong place a strong emphasis on compliance and risk assessment. Your credit history and financial background can directly influence your eligibility to open a current account, especially for corporate or premium accounts. For companies, banks often assess the directors’ and shareholders’ profiles, business activity, and financial standing. A solid credit record improves your chances of approval, while a weak or limited history may result in restricted services or additional documentation requirements.

3. Packaged Benefits with Premium Current Accounts

Many banks in Hong Kong offer packaged current accounts that go beyond basic banking services. These may include:

- Travel or health insurance coverage

- Reward programs tied to spending or deposits

- Preferential FX rates for frequent international transfers

- Dedicated relationship managers for business clients

While these perks can add value, it’s important to weigh the monthly fees or minimum balance requirements against the actual benefits to ensure the account suits your financial needs.

Conclusion

In Hong Kong’s dynamic financial landscape, current accounts are an essential tool for both individuals and businesses to manage day-to-day transactions efficiently. From monitoring balances and setting up direct debits to navigating FX fluctuations and understanding credit requirements, choosing the right current account ensures smooth operations and compliance with local regulations. By selecting a bank and account type that aligns with your financial needs, you can optimize cash flow, protect funds, and maintain transparency in all financial dealings.

How FastLane Group Can Help

Opening a current account in Hong Kong can be a complex process, especially for foreign entrepreneurs and companies. FastLane Group simplifies this journey with expert guidance on bank selection, account setup, and regulatory compliance. Our professional team ensures that your banking and corporate structure are tailored to your business objectives, helping you save time, reduce administrative hurdles, and focus on growth. Whether you are establishing a personal account or a company account, FastLane Group provides end-to-end support to streamline your financial operations in Hong Kong. Contact us now for a consultation!

FAQs on Current Accounts in Hong Kong

1. Can foreigners open a Hong Kong current account?

Yes, foreigners can open a current account in Hong Kong, but the process may require additional documentation such as proof of identity, residential address, and details about your source of funds. Banks also conduct due diligence checks to comply with local anti-money laundering regulations. Working with a professional service like FastLane Group can simplify the application process.

2. How long does it take to open a business account?

Opening a Hong Kong business current account typically takes 2 to 6 weeks, depending on the bank and complexity of your company structure. Banks often require submission of incorporation documents, business plans, and proof of beneficial ownership. Delays may occur if additional verification is needed for foreign directors or shareholders.

3. Which is better for SMEs — local banks or virtual banks?

Local banks offer traditional banking services with branch access and a wide range of corporate products, which is ideal for businesses with high transaction volumes. Virtual banks provide faster onboarding, lower fees, and convenient online banking, making them suitable for small and medium enterprises (SMEs) focused on digital operations. Choosing the right option depends on your business needs and cash flow management preferences.

4. What documents are needed for expats vs companies?

- For expats: Valid passport, proof of residential address (utility bill or bank statement), employment details, and sometimes a reference letter from your home bank.

For companies: Certificate of Incorporation, Business Registration Certificate, Articles of Association, proof of directors and shareholders, and a resolution approving account opening. Banks may request additional information for foreign-owned companies to comply with regulatory requirements.